YETI Holdings, Inc. $YETI

YETI Holdings, Inc. $YETI

My Investment Checklist

1. Is the company undervalued?

EV/EBIT: 16.34

EV/Sales: 3.01

Price/Book: 9.64

$YETI has nearly 10X’d sales since 2014 and trades at a reasonable valuation. However these metrics are backwards looking and there’s reason to believe growth will decelerate moving forward. Nonetheless $YETI is throwing off tons of free cashflow and should continue to grow for some time. The business is also incredibly profitable, which makes $YETI an interesting idea.

2. Can I easily explain what the company does?

Yes, they are an omni channel retailer who sell outdoor goods. 63% of sales comes from drinkware ie; tumblers, 35% comes from coolers, and 2% from miscellaneous branded merchandise.

3. Does the cash flow statement line up with income statement?

Yes, cashflows while choppy have been higher than reported earnings:

Most of their excess cash went towards inventories, share repurchases, and capital expenditures. The build up of inventories is a pretty big red flag, especially considering that number is up 125% YOY. Management did state that two thirds of this inventory was in transit, but that’s not a satisfactory answer IMO. Sales were only up 19% YOY in Q1 and the only logical explanation for this discrepancy is management overestimating demand.

Other than that, I don’t have any issues with the capital allocation decisions $YETI made last year.

4. Is the Balance Sheet Healthy?

Total Debt: $106.9M (This excludes operating leases and deferred financing)

Total Cash: $100.3M

Current Ratio: 1.82

$YETI only paid ~$3.3M in interest expenses last year and have virtually zero net debt. This coupled with strong FCF, gives $YETI a nearly perfect balance sheet grade.

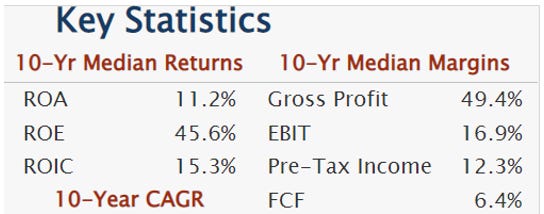

5. How profitable is the business?

Gross Margins: 56.7%

Operating Margins: 18.4%

Net Margins: 14.3%

As you can see $YETI is a high quality business, which reflects a moat surrounding their brand. Howeva it wouldn’t be a stretch to conclude that $YETI is over earning:

What’s even more troublesome is that profitability has been all over the place. For example EBIT margins were 16.9% in 2013, 27.3% in 2015, 10% in 2017, and 19.6% in 2020. $YETI is a far cry from a predictable business, but even in trough years margins remain solid.

6. What is the company’s growth potential?

9-yr Revenue CAGR: 35.77%

9-yr Operating Profit CAGR: 38.15%

9-yr FCF CAGR: 32.98%

Breathtaking numbers here and all done without acquisitions! With that said, $YETI is a much larger company now and growth will certainly stagnate moving forward. Although management is still forecasting 19% topline growth in 2022. Furthermore $YETI is growing rapidly in international markets, introducing new products, and expanding their direct-to-consumer marketing. For these reasons I would anticipate $YETI to continue growing double digits in the near term.

7. Is management rewarding shareholders?

$YETI doesn’t offer a dividend, but just repurchased $100M worth of shares. Interestingly when asked about capital allocation, management stated they plan on reinvesting back into the business, then looking for M&A targets, and then opportunistically returning capital via buybacks. This grabbed my attention because $YETI barely has any debt and are expected to print north of $150M in FCF over the next 12 months. Moreover the recent buybacks were done at an average price of just under $60/share. Their stock is now ~16% cheaper, so I don’t understand why the C-Suite wouldn’t double down on share repurchases??? The opportunity is objectively much better now and management all but said their putting buybacks on the shelf for the time being. Additionally $YETI has never done an acquisition as public company, which leads me to believe that management and shareholder interests are not aligned.

8. How does the company stack up against their peers?

There’s really no apples to apples competitor for $YETI, so I’m gonna be lazy and skip this question.

9. What’s the counter argument?

The counter argument is that sales will slow as $YETI offers a discretionary product in an inflationary/recessionary environment.

I totally buy into this thesis, the buildup of inventories alone is an admission of slowing demand. Furthermore a decent chuck of revenues come from corporate sales ie; Coca-Cola putting their logo on a Yeti cup for employees. There’s recently been sizable layoffs in corporate America, so it wouldn’t surprise me to see these sales fall off a cliff. Finally the products they sell are extremely durable, so an average customer is only going to purchase a few coolers in their entire lifetime.

10. Is there something I think the market may be missing?

This is going to be a spicy take, but I think Yeti is a fad! I don’t understand why you would require a cooler to keep your beers cold for 6 days straight or why you need a tumbler to chill your beverage all day long?!?!? That seems wildly unnecessary, when you can buy a slightly lower quality product for 75% less.

I think Yeti’s “coolness” factor is what’s causing consumers to pay a high price for a product that’s more or less a commodity. And as guy who peaked in high school I can assure you; popularity is fleeting.

Final Thoughts:

I’m not gonna lie I hate $YETI, chiefly because I no idea what this business will look like in 10 years. In fairness I’m not an outdoors man so I definitely could be overlooking Yeti’s competitive advantage. Additionally management is throwing off some serious used car salesman vibes. Their capital allocation decisions would at best suggest incompetence and at worst imply nefarious intent. For these reasons $YETI is a hard pass and something I won’t revisit unless the valuation gets out of this world compelling.

***Disclosure: I have no position in the security mentioned above, nor do I have any plans to purchase within the next 72 hours. This article is intended for educational purposes only and in no way should be interpreted as investment advice