Whirlpool Corporation $WHR

Whirlpool Corporation $WHR

My Investment Checklist

1. Is the company undervalued?

EV/EBIT: 6.3

EV/Sales: 0.66

Price/Book: 2.37

Whirlpool is a solid company with pricing power that’s trading near an all-time low valuation. Moreover the company throws off tons of free cash flow and returns the lion’s share of those profits back to shareholders. However the appliance business is low to no growth by nature and can be quite cyclical. Investors are concerned future demand has already been pulled forward and for that reason the stock is priced appropriately. Conversely management is steadfast in their assertion that demand remains strong and if this proves to be true, $WHR shareholders will likely see outsized returns.

2. Can I easily explain what the company does?

Yes, they are an appliance manufacturer ie; ovens, refrigerators, stand mixers, washing machines, etc… They sell mostly to household consumers, but also have a commercial offering.

3. Does the cash flow statement line up with income statement?

Yes, while choppy cashflows have on net been higher than reported earnings:

Most of their excess cash went towards buying back stock, inventory expenses, capital expenditures, debt repayment and dividends paid out. The increase in inventory strikes me as problematic and a potential warning sign. For example, last quarter inventories were up ~17% YOY, while sales were down ~8% YOY. Furthermore management’s explanation was a combination the War in Ukraine and supply chain issues. Both of the aforementioned reasons strike me as a convenient scapegoat to cover up underlying business weakness. With that said it could simply be a noisy quarter, but something I would keep an eye on in the future.

4. Is the Balance Sheet Healthy?

Total Cash: $2.11B

Total Debt: $6.21B

Current Ratio: 1.14

$WHR does hold a meaningful amount to debt relative to their market cap and paid $171M last year in interest expenses. With that said Whirlpool is a free cash flow machine and expected to do over $2.1B in operating income in 2022. That works out to almost 12.5X interest coverage, which is phenomenal. Even if the business deteriorates massively, the balance sheet shouldn’t be a concern for investors.

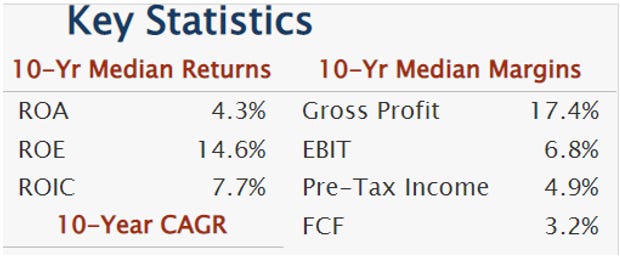

5. How profitable is the business?

Gross Margins: 19.1%

Operating Margins: 10%

Net Margins: 7.7%

Cleary $WHR isn’t a wonderful business, but I wouldn’t characterize it as bad either. It’s also important to note that the trailing data implies Whirlpool may be over earning:

Notwithstanding management thinks they can achieve 11.5% EBIT margins long term. I also don’t think this a farfetched ambition, as some previously unprofitable business units have inflected profitably in recent years. Additionally management has hinted they may sell off their Europe, Middle East, and Africa segment as it’s currently hemorrhaging money. This coupled with a price increase about to kick in makes me think the business has a structurally improved margin profile.

6. What is the company’s growth potential?

10-yr Revenue CAGR: 1.7%

10-yr Operating Profit CAGR: 7.51%

10-yr FCF CAGR: 17.75%

FCF growth is overstated here due to the start and end dates used. Nevertheless, $WHR is not a compounder by any stretch of the imagination. However it’s not a melting ice cube either:

While 2% growth is anemic, it’s moving in the right direction and has been fairly predictable for the last 70 years. Given the present valuation $WHR doesn’t need to tear the cover off the ball to delivery satisfactory returns.

7. Is management rewarding shareholders?

Whirlpool currently offers investors a 3.86% dividend and have $2.9B remaining on their share repurchase program. On top of this management intends on returning $1.5B back to shareholders in 2022. Unfortunately, that’s not a sustainable number IMO as $WHR only anticipates $1.25B in FCF for the fiscal year. I believe $1B would be a more reasonable number to assume moving forward, which works out to a ~9.6% total shareholder yield. It should go without saying that a 9.6% cash return is phenomenal!!

8. How does the company stack up against their peers?

I couldn’t find a pure play appliance manufacturer to compare with $WHR so I’m gonna skip this question. Also don’t even think about buying $GE, that business blows!

9. What’s the counter argument?

By far the biggest counter argument is that $WHR is at a cyclical peak in earnings. Bears would content that the optically low multiple will prove to be correct once earnings start contracting.

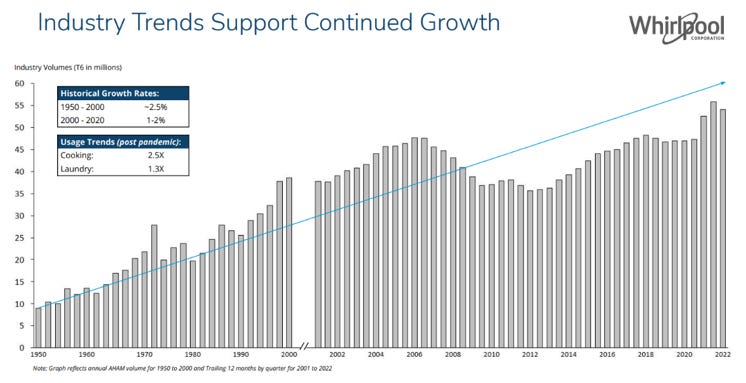

I’m inclined to buy into this thesis, as homeowners can hold off buying a new washing machine for a year or two if needed. Also it’s impossible to believe that government stimulus hasn’t contributed to a pull forward in demand. Nonetheless management is adamant that demand remains “robust” (I can’t stand that word). They are guiding for 2-3% growth this year and 5-6% organic growth per year long term.

I honestly have no clue, gun to my head I would say management is over extrapolating demand. I really can’t get over that fact that Whirlpool’s inventories built up while sales declined simultaneously. Fortunately investors will have a better understanding of demand in a quarter or two as government funny money dries up.

10. Is there something I think the market may be missing?

As mentioned previously Whirlpool’s management team seems focused on improving profitability and making their organization leaner and meaner. They’ve done this by transforming money losing businesses into profitable ones. As well as implementing long term cost savings initiatives and investing heavily into higher returning business units. If management executes, mid-single digit earnings growth is more than achievable.

Final Thoughts:

My base case as follows; flat earnings for 2022 and then growing at 3% per year thereafter, a 9.5% total shareholder yield annually, and a 9X EV/EBIT exit multiple in 5 years. That works out to a ~19.5% expected IRR, which is extremely attractive. Unfortunately I don’t have a lot of conviction in that earnings estimate. Candidly the range out outcomes are fairly wide and I wouldn’t be surprised to see earnings contract over the next couple of years. If so, the stock is probably priced appropriately and shareholder yield will be the only form of compensation for investors. Although it’s worth tracking, as the stock offers a phat right tail payoff if management can delivery on the promises they’re making.

***Disclosure: I have no position in the security mentioned above, nor do I have any plans to purchase within the next 72 hours. This article is intended for educational purposes only and in no way should be interpreted as investment advice