Weber, Inc. $WEBR

My Investment Checklist

1. Is the company undervalued?

EV/Sales: 0.84

$WEBR doesn’t show up on any value screen and the company is facing a myriad of issues. They’re losing money, demand has plummeted, recently cut their dividend, and have liquidity/debt problems. Nevertheless, $WEBR is the #1 brand in their category and have historically grown at an above market rate. If $WEBR can navigate thru this turbulent period, investors could be compensated for buying into a terrifying situation.

2. Can I easily explain what the company does?

Yes, they sell grills and grill accessories internationally.

3. Does the cash flow statement line up with income statement?

No reported income hasn’t come close to lining up with their cashflows:

Most of their cash went towards inventory buildup, capital expenditures, and “other operating activities”. Upon further investigation the other operating activities appears to be; a tax expense, prepaid expenses, and a change in payables/accrued expenses. My instinct is to call BS here as $171.5M in the last 12 months on other operating activities seems like an absurd amount for a business valued at $343M. I could be wrong, but I’d be willing to bet there’s a lot of pork in those line items.

4. Is the Balance Sheet Healthy?

Total Cash: $40.8M

Total Debt: $1.2B

Current Ratio: 1.4

This is a frightening balance sheet for a company that’s losing money and experiencing a business slow down. $WEBR also issued ~$400M of net debt over the last 7 quarters, which further exacerbates their problem. They paid $69M last year in interest expenses, which is bound to go up and any debt they roll will surely be at a much higher rate. The only saving grace here is that inventories are elevated, so free cash flow should be pretty solid near term.

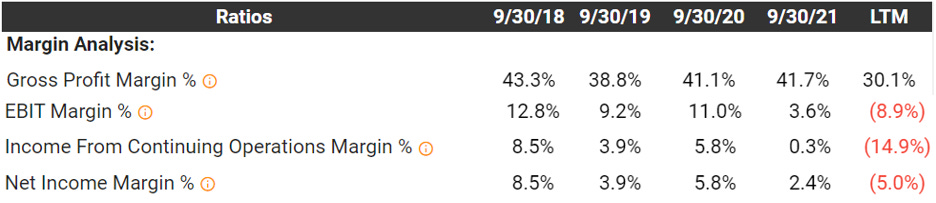

5. How profitable is the business?

Gross Margins: 30.1%

Operating Margins: (8.9%)

Net Margins: (5%)

Again extremely difficult to get excited about these results. However $WEBR is going thru a bad year, so profitability should be below trend. Moreover there’s not a lot of historical data to go on, but here’s what they’ve done over the last 4 years:

As you can see under normal circumstances $WEBR isn’t a bad business at all (I would argue above average). Being such a durable brand $WEBR does have pricing power, although not during trough periods. For example, in their latest earnings call management stated that they plan on eating any and all input costs for the time being. Nevertheless tough times don’t last forever and the sun will eventually shine on Weber’s profit margins. Moreover management is making a well-articulated case for higher profits moving forward:

6. What is the company’s growth potential?

4-yr Revenue CAGR: 10.28%

It’s difficult to analyze growth with only 4 years of data, one of which being an unprofitable year. However the business is no doubt growing organically:

I wouldn’t expect double digit growth as my base case moving forward, but $WEBR should grow mid-high single digits over the long term.

7. Is management rewarding shareholders?

$WEBR recently cut their dividend and have no capital return policy in place. I actually give management credit here, as dividend cuts are universally seen as unpopular. Although this was done out of necessity, so I’m only willing to give so much credit. Furthermore Weber’s leverage ratios are absurdly high and any free cash flow generated over the next 3 years should go directly to debt reduction. It’s also important to note that $WEBR issued ~29% of their current market cap in stock based compensation ($102M) last year and sold $213M (net) worth of shares on the open market. If $WEBR can’t turn a profit quickly, shareholders will almost certainly get more dilution than they bargained for.

8. How does the company stack up against their peers?

Trager, Inc. $COOK is the closest competitor to $WEBR

$COOK EV/Sales: 1.05

Gross Margins: 36.4%

Operating Margins: (14.8%)

$COOK is slightly more expensive than $WEBR, but they have a less awful balance sheet and better gross margins. Additionally both companies are diluting shareholders massively and have big time liquidity problems. Picking between these two is like answering a would you rather question. Frankly I would rather avoid both like the plague.

9. What’s the counter argument?

The counter argument is that chapter 11 isn’t far off, as $WEBR is burning thru money, getting squeezed by inflation, and demand has fallen off a cliff.

I totally buy into this thesis, there are so many ways for this investment to back fire and an exceedingly narrow path for excess returns. I will say $WEBR is an extremely durable brand, that I assume will be around 20 years from now. Additionally the company should be able to throw off some free cash flow, but paying off their liabilities will take years if not decades.

10. Is there something I think the market may be missing?

I don’t think the market is missing anything here, if anything $WEBR seems expensive. The company has a very real chance of being a doughnut and they’re still priced at 0.84X EV/Sales. For context I own businesses with a net cash position that are trading at a lower multiple.

Final Thoughts:

This should come as no surprise, but $WEBR is a hard pass. There’s no need to be a hero and bet on a highly leveraged cyclical in this market. With that said I would revisit the name if their business turned around materially and debt got down to a palatable level.

***Disclosure: I have no position in the security mentioned above, nor do I have any plans to purchase within the next 72 hours. This article is intended for educational purposes only and in no way should be interpreted as investment advice