VMware, Inc. $VMW

My Investment Checklist

1. Is the company undervalued?

EV/EBIT: 19.6

Price/Sales: 4.16

Price/Book: 5.11

$VMW is a wonderful business, which trades at a slight discount to the market. The company has historically compounded at a fast rate and is guiding for high single digit growth in the future. This coupled with a generous share repurchase plan, makes $VMW a compelling investment opportunity.

2. Can I easily explain what the company does?

VMware is a cloud computing and services business, who market chiefly to enterprise clients. The VW in VMware stands for virtual machines and they essentially offer outsourced server solutions for third party businesses.

Candidly I only have a high-level understanding regarding their product offerings and competitive advantage in the marketplace. With that said most of their revenue comes from recurring subscriptions, so there’s no doubt a switching cost moat.

3. Does the cash flow statement line up with income statement?

Yes cashflows have been significantly higher than reported earnings, which is lovely to see:

Most of their cash went towards share repurchases, capital expenditures, and a small amount for the acquisition of Mesh7 in March of 2021. These seem like intelligent capital allocation decisions, however I’m a bit underwhelmed. For instance, $VMW had ~$4.2B in free cashflow and issued $5.6B in net debt over the last 12 months. The aforementioned expenses only add up to ~$1.7B, which leaves a significant amount of cash sitting idle. In fairness $VMW did just complete their spin off from Dell in November, so perhaps management gets more judicious with their capital in the future.

4. Is the Balance Sheet Healthy?

Total Debt: $11.73B

Total Cash: $12.53B

Current Ratio: 1.58

FORTRESS BALANCE SHEET!!!!

5. How profitable is the business?

Gross Margins: 82.41%

Operating Margins: 20.67%

Net Margins: 16.05%

ROIC: 11.75%

These metrics are outstanding and why I consider $VMW to be a wonderful business. Furthermore, the trailing data is an accurate reflection of how the company has performed historically:

There’s really nothing negative I can say here, $VMW is elite and will likely continue being elite!!!

6. What is the company’s growth potential?

10-yr Revenue CAGR: 15.2%

10-yr EBIT CAGR: 12.7%

10-yr FCF CAGR: 14.6%

Again $VMW is putting up impressive numbers, although their future prospects aren’t as promising. For example, VMware is guiding for 9% revenue growth and a ~8% decline in free cash flow for 2022. Moreover analysts are only forecasting 8% sales growth out into the future. Nonetheless 8% growth is nothing to sneeze at and it wouldn’t shock me if VMware ends up growing at double digits for the next few years.

7. Is management rewarding shareholders?

$VMW has a $2B share repurchase plan in place until the end of 2024. They also bought back ~$1.3B in shares over the past 12 months. On its face that seems impressive for a $52B company, however $VMW also issued over $1B in stock-based compensation. Furthermore the company has a long history of issuing copious amounts of SBC. When factor in stock-based compensation, shareholder yield is essentially nonexistent. For example, the diluted share count has only gone down by 0.21% per year since 2011.

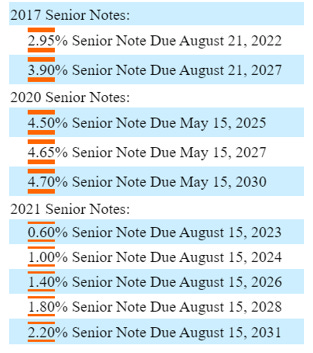

Nevertheless $VMW isn’t diluting shareholders and giving their employees equity in the business seems like a smart way to align incentives. Finally $VMW is sitting on a giant cash cushion and have absurdly low coupons on their outstanding debt:

With growth starting to slow, I would not be surprised if $VMW accelerates share repurchases while continuing to roll their debt.

8. How does the company stack up against their peers?

VMware’s top competitors are Microsoft $MSFT and Oracle $ORCL

$MSFT Price/Sales: 13.57 $ORCL Price/Sales: 6.19

EV/EBIT: 29.53 EV/EBIT: 25.87

Operating Margin: 38.52% Operating Margin: 27.21%

$ORCL is significantly more expensive than $VMW and has barely grown so we can eliminate them easily. $MSFT is also incredibly expensive, but have recently grown faster than VMware and have a deeper moat. With that said Microsoft’s margins are the fattest they’re ever been and more likely than not to contract from here IMO. Furthermore I have a hard time getting behind a business that thinks it’s a good idea to repurchase their share at 13X sales. Sorry FANMAG fans boys, but 13X sales for a mature $2.3T company is a borderline insane price to pay. Finally $VMW actually has a higher trailing 10-yr revenue CAGR than $MSFT, which makes VMware the no brainer choice here.

9. What’s the counter argument?

The counter argument is that there’s a reason why Dell thought it was a good idea to spin off VMware. In other words competition is about to take market share, which will lead to a downward spiral.

I really can’t speak intelligently to the competition argument, I’m not a tech nerd and don’t know how good VMware’s offering is compared to their competitors. Having said that, literally every business faces competition and the financial metrics are by no means deteriorating in a material way.

Additionally Michael Dell, the founder of $DELL is still a majority owner in $VMW. This could obviously change in the future, but it’s been overs 3 months since the spin off. If Mr. Dell was truly that pessimistic, he would’ve likely sold some shares by now.

10. Is there something I think the market may be missing?

$VMW shareholders were awarded a $27.40 special dividend in November, as a result of the Dell spin off. Since that time, the share price has dropped by ~ $44. This is a perplexing move by Mr. Market when you consider that the special dividend came from $DELL and not $VMW. Moreover there’s been no impactful news since then and VMware’s last quarter of earnings were pretty good IMO. I have no explanation for this other than market participants acting irrationally.

Final Thoughts:

$VMW has historically traded in the 20-35X EV/EBIT multiple range, which makes sense given their impressive growth and profitability metrics. Considering that VMware is expected to grow at a slower rate 25X seems like a fair multiple, which gives a ~30% margin of safety. If you assume 8% growth, zero net shareholder yield, and a 25X EV/EBIT exit multiple; you would be looking at a 16.5% expected return over 3 years. That’s pretty good and what I would consider to be my base case. Unfortunately it’s not a business I understand well and I think there are better opportunities elsewhere. Although it’s a stock I’ll watch closely, as my assumptions may be too conservative and management likely has some additional breadcrumbs to share with investors now that they’re operating autonomously.

***Disclosure: I have no position in the security mentioned above, nor do I have any plans to purchase within the next 72 hours. This article is intended for educational purposes only and in no way should be interpreted as investment advice