Turning Point Brands, Inc. $TPB

Turning Point Brands, Inc. $TPB

My Investment Checklist

1. Is the company undervalued?

EV/EBIT: 12.01

Price/Sales: 1.73

Price/Book: 5.48

$TPB is a high-quality business, which trades at a significant discount to the market. Furthermore, the company has a long runway for growth as more states start to decriminalize/legalize marijuana. Unfortunately this is a sin stock so there’s a decent amount of regulatory uncertainty, chiefly surrounding $TPB’s vaping business. If however these headwinds turn out to be a nothing burger, then $TPB offers an incredibly asymmetrical bet.

2. Can I easily explain what the company does?

Yes; they sell joint papers, dipping tobacco, and vape products.

3. Does the cash flow statement line up with income statement?

Yes, cashflows have for the most part been higher than reported earnings:

Most of their free cashflow went towards paying off debt, the acquisitions of Unitabac Cigar and Direct Value Wholesale, as well as share repurchases. $TPB’s acquisitions make sense to me as they have no market share in the cigar/cigarillo space. Although, they took out an 8% loan in order to complete these transactions and added $2.5M of “goodwill” to their balance sheet. I’m extremely skeptical that these synergies will create $2.5M of value for $TPB’s business, but they didn’t pay an outrageous price and $2.5M only accounts for ~3% of the company.

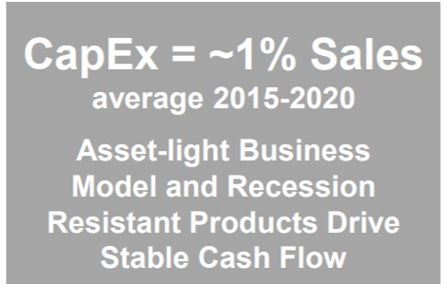

On a brighter note, $TPB is a free cash flow machine with absurdly low capital expenditure requirements:

Moving forward $TPB should be able to fund acquisitions out of free cash flow and not debt, which of course is wonderful for equity owners!

4. Is the Balance Sheet Healthy?

Total Cash: $130.55M

Total Debt: $438.4M

Current Ratio: 4.90

$TPB holds a sizeable amount to debt relative to their market cap. However the company is practically printing cash and only paying $21M a year in net interest expenses. This coupled with a considerable cash cushion gives $TPB a good, but not great balance sheet.

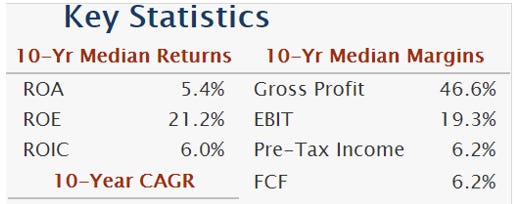

5. How profitable is the business?

Gross Margins: 49.27%

Net Margins: 11.19%

ROIC: 13.82%

7-yr Revenue CAGR: 11.17%

While $TPB may not offer software like margins, they’re objectively above average across the board! Additionally this performance is fairly consistent with what they’ve done historically:

Moreover it wouldn’t be unreasonable to assume margins expand from here, as $TPB has elite brands and pricing power IMO. Any way you slice it, $TPB is an outstanding business!

6. Is management rewarding shareholders?

$TPB currently offers a 0.55% dividend and recently increased their share repurchase plan to up to $50M. Unfortunately there was no time table given to complete these buybacks. However $TPB’s stock recently nose-dived after earnings, so I would anticipate a good chuck of that $50M to be put to work shortly. Moreover $TPB spent over $23M in buybacks last year and is guiding for ~ $105M in operating income this year. I think it’s safe to assume at least $30M in share repurchases over the next 12 months, which would equate to a ~4.5% total shareholder yield. This is outstanding for a company which is still growing at a high rate!!!

7. How does the company stack up against their peers?

I could compare $TPB to an Altria $MO or British American Tobacco $BTI, but I won’t. $TPB doesn’t sell cigarettes and shouldn’t be lumped in with every other tobacco manufacturer. In fact, I would argue it’s a hedge against cigarettes, as vaping accounts for roughly 1/3 of sales.

There’s no publicly traded company I could find with a similar business model, so for that reason I’m gonna be lazy on this question.

8. What’s the counter argument?

By far the biggest counter argument is the regulatory uncertainly surrounding $TPB’s vape business. In short, $TPB doesn’t know if they will get approval for some of their existing vape products and is reducing exposure as a result.

I no idea how the FDA will rule regarding $TPB’s vape enterprise and would concede that there’s a chance the entire business segment could be a doughnut. Having said that the FDA rescinded their Marketing Denial Order on 10/7, which allows $TPB to conduct business as usual. Moreover $TPB’s management team made the following statement on their last earnings:

“We are encouraged by the FDA’s decision to reconsider and place back into review our application for our proprietary vapor products. I am confident that we submitted a robust application…”

In fairness there’s a 0% chance they would say we’re totally screwed here, but I think the language would be more vague if management was less optimistic. I mean c’mon the application they submitted wasn’t mediocre, it was robust!

9. Is the company unsexy, uncool, or contrarian?

$TPB has 6 analysts covering the stock with; 1 sell, 1 underperform, and 4 hold ratings out. Furthermore it’s a sin stock so unless you’re a stoner bro, the stock is unsexy, uncool, and contrarian.

10. Is there something I think the market may be missing?

As mentioned previously $TPB’s stock sold off over 20% after reporting Q3 earnings. However their vaping segment only comprises ~5% of operating earnings:

There’s no universe in which that makes sense and you’re a complete shithead if you buy into the efficient market hypothesis. Everything else on that earnings report was specular, so I have no conclusion other than Mr. Market wayyyyy over reacting.

Final Thoughts:

$TPB is a great business that trades at a bargain with a competent management team. Furthermore it doesn’t take a stock market genius to figure out this company can grow sustainably for years to come. Having said that it’s difficult to forecast out future growth, but their other business segments are growing at double digits and mid-high single digits respectively. To be conservative I would assume earnings grow by at least 6% per year for the foreseeable future. Additionally $TPB has traded all over the place; ranging from a 10-25 X EV/EBIT multiple since 2017. Intuitively 15X seems like a fair price, given that the company is above average in regards to margins, shareholder yield, and revenue growth.

Bringing this full circle I would expect 6% earnings growth, a 4.5% shareholder yield, and a 15X EV/EBIT multiple re-rate in the next few years. If this happens shareholders would receive a 18.22% CAGR!!! I would also consider this to be my base case, as the assumptions used here are towards the lower end of $TPB’s historical averages.

In closing I’m strongly considering starting a position, as this is a company I can own for a long time while their earnings compound. Additionally there’s a massive right tail payoff if nothing comes of the FDA uncertainty and $TPB keeps growing at double digits. With that said, I usually like to let investment ideas marinate in my brain for a month or so. If I still have warm and fuzzies in a few weeks, then I’ll probably establish a position.

***Disclosure: I have no position in the security mentioned above, nor do I have any plans to purchase within the next 72 hours. This article is intended for educational purposes only and in no way should be interpreted as investment advice