The Container Store Group, Inc. $TCS

The Container Store Group, Inc. $TCS

My Investment Checklist

1. Is the company undervalued?

EV/EBIT: 7.57

Price/Sales: 0.6

Price/Book: 1.67

$TCS trades at a massive discount to the market, while performing exceptionally well over the last 12 months. However management and analysts are forecasting earnings to decline in the near term and potentially further out. Be that as it may, investors could achieve outsized returns as growth isn’t expected to fall drastically and the stock could see a massive multiple re-rate.

2. Can I easily explain what the company does?

Yes, they design and install custom closets as well as selling household storage solutions ie; shoe racks.

3. Does the cash flow statement line up with income statement?

Yes, cashflows have been consistently higher than reported earnings:

Almost all their free cashflow went towards paying off debt and capital expenditures. I would like to see some shareholder return, but there’s nothing unusual about these capital allocation decisions.

4. Is the Balance Sheet Healthy?

Total Debt: $494.8M

Total Cash: $23.14M

Current Ratio: 1.12

$TCS holds a lot of debt relative to their market cap. However over $285M is coming from long term lease obligations, which is overstating their total debt burden. Furthermore $TCS is only paying $14.2M in net interest payments, which is likely to go down in the coming years. Considering $TCS’ strong cashflow, the balance sheet is quite manageable and slightly above average IMO.

5. How profitable is the business?

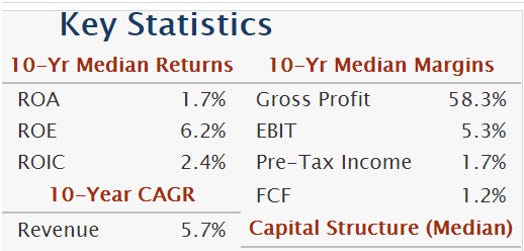

Gross Margins: 59.03%

Operating Margins: 13.51%

ROIC: 12.43%

10-yr Revenue CAGR: 5.7%

At first glance these numbers look pretty solid, but the trailing 12 month data is painting an overly optimistic picture:

While gross margins hold up, ROIC and operating margins are materially worse. For example from 2012-2020 operating margins ranged from 6.5-3.1%. This is a huge drop off and it would be foolish to extrapolate double digits margins for $TCS into the future.

Notwithstanding their revenue growth has actually been remarkably consistent and $TCS has grown every year for the past decade. All in all $TCS is not a great business, but also not gross at the same time.

6. Is management rewarding shareholders?

$TCS doesn’t offer a dividend or buy back shares. In fairness they also don’t dilute shareholders (other than thru stock-based compensation). However this is a bit disappointing given the strong free cash flow generation and low present valuation.

7. How does the company stack up against their peers?

$TCS is an incredibly unique business, I could compare them to a home goods retailer like Bed Bath and Beyond $BBBY, but I think that would be a waste of time. For that reason I’m skipping this question.

8. What’s the counter argument?

The counter argument is the $TCS’ earnings are at a cyclical peak, which will normalize over the next few quarters.

I’m inclined to buy into this narrative, as margins have almost tripled from 2020. If you apply a 5% operating margin on last year’s revenue, EBIT drops from ~$150M to ~$55.5M. That’s a massive difference and likely the reason for such a compressed valuation.

9. Is the company unsexy, uncool, or contrarian?

$TCS has 6 analysts covering the stock with 4 holds and 2 buy ratings out. For this reason the stock is definitely not contrarian. However the stock is certainly unsexy and uncool as they sell storage solutions, my apologies Jay Pritchett!

10. Is there something I think the market may be missing?

As mentioned previously management is forecasting sales to decline by 5% in the next quarter and earnings to shrink to $0.20/share. That’s more than a 50% decline in earnings YOY. However management may be low balling this number on purpose to play a mind game with analysts and make themselves look good when earnings are “only” down 30% YOY.

Moreover $TCS has the potential to grow for years to come at a $665M market cap and only 94 stores open currently.

Final Thoughts:

$TCS seems interesting, given the history of consistent revenue growth and strikingly low valuation. However the company is giving zero shareholder yield and expected to have earnings fall drastically in the future. This means $TCS investors are playing a multiple re-rate game, which is an extremely difficult one to get right. For that reason it’s a pass, but I may revisit if management starts returning capital back to shareholders and the stock remains undervalued.

***Disclosure: I have no position in the security mentioned above, nor do I have any plans to purchase within the next 72 hours. This article is intended for educational purposes only and in no way should be interpreted as investment advice