The Chef’s Warehouse, Inc. $CHEF

My Investment Checklist

1. Is the company undervalued?

EV/EBIT: 27.55

EV/Sales: 0.81

Price/Book: 73.7

On the surface $CHEF doesn’t appear undervalued, however on a forward basis the company is trading at a modest multiple. Furthermore $CHEF is growing at a ridiculous clip and should see margin expansion. Conversely it’s objectively a gross business and most of their growth has been inorganic. Nevertheless if $CHEF can keep compounding at 15%+ annually, there’s a lot of ugliness I’m willing to overlook.

2. Can I easily explain what the company does?

Yes, they are a specialty foods distributor. In other words they sell food to restaurants and catering companies.

3. Does the cash flow statement line up with income statement?

Yes, more red than I would like to see but cashflows have been less negative than reported earnings:

In the last 12 months $CHEF has spent over $55M on acquisitions. Their biggest outside purchase was for Capital Seaboard, a seafood distributor in Maryland. The company was acquired for ~$31M. Moreover thru the first 2 quarters of 2022 Capital Seaboard posted over $70M in sales and $2.89M in EBIT. Even if those numbers taper off in the back half of the year, it would appear as if this deal was highly accretive for shareholders. Additionally management does have a solid track record with acquisitions and there appears to be natural synergies with their core business. For these reasons I’m willing to give management the benefit of the doubt.

The remaining expenses were capital expenditures and inventories. I have no issues here, as revenue growth accounts for the increase in inventories.

4. Is the Balance Sheet Healthy?

Total Cash: $51.8M

Total Debt: $392.8M

Current Ratio: 2.07

$CHEF holds some debt relative to their market cap and paid a little over $17M in interest expenses last year. That works out to less than a 4X net interest coverage ratio, which is not great. However operating earnings are expected to grow by ~50% in the next 12 months, which gives shareholders some breathing room. All in all not a great balance sheet, but growth should improve creditworthiness in due time.

5. How profitable is the business?

Gross Margins: 23.1%

Operating Margins: 2.9%

Net Margins: 1.4%

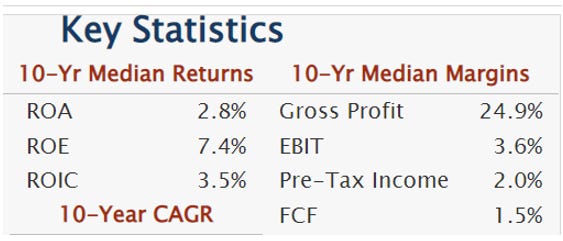

As mentioned previously $CHEF is a gross business, but that shouldn’t surprise anyone as they’re a glorified middle man. With that said $CHEF is probably under earning based on historical numbers:

Furthermore $CHEF has two new facilities, which will likely improve efficiencies and cut down on transportation costs. Additionally inflation is finally starting to abate, so that should naturally lead to less pressure on input costs and higher profitability.

6. What is the company’s growth potential?

10-yr Revenue CAGR: 15.9%

8-yr Operating Profit CAGR: 7.31%

8-yr FCF CAGR: 27.99%

I chose to look at 8-year CAGR’s for bottom line metrics, in order to eliminate the noise of Covid-19. Nonetheless incredibly impressive numbers here, although there’s been quite a bit of M&A. However this is not to suggest that $CHEF doesn’t grow organically:

Double digit grow is hard to come by and that’s what makes $CHEF an interesting investment idea.

7. Is management rewarding shareholders?

Management does not offer a dividend or repurchase shares. In fact, they’re dilutive to shareholders by issuing stock based compensation and convertible debt. Candidly I’m a sucker for shareholder yield. Although Chef’s Warehouse does seem proficient in the art of M&A and if they can keep buying companies for 6X EBIT, I doubt there would be a better use of capital.

8. How does the company stack up against their peers?

$UNFI is probably the closest competitor to $CHEF:

$UNFI EV/Sales: 0.22

EV/EBIT: 13.37

Operating Margin: 1.6%

$UNFI is much cheaper than $CHEF and has grown at more or less the same rate. Conversely it also holds substantially more debt and is more capital intensive. I don’t think there’s a clear winner here, but I will say $UNFI is probably riskier with a higher potential return.

9. What’s the counter argument?

The counter argument is that profitability will continue to be a drag as inflation is still hot and dining out will likely contract in a recessionary environment.

These are logical arguments, but I think the bottom is already in. While dining out may see a pull back, catering events are likely to see a massive jump YOY. Furthermore there very well could be deflation on input costs such as meat and cheese. In short, I would be surprised if margins are lower a year from now.

10. Is there something I think the market may be missing?

There’s been significant consolidation in the food distribution industry. This almost always piques my interest as consolidation means less competition. The company will no doubt have to keep executing, but they may have a structurally improved margin profile as a result. It wouldn’t be ludicrous to forecast out a 5% EBIT margin over the next few years. If that scenario plays out $CHEF is trading at too low a price.

Final Thoughts:

My base case for $CHEF would be 12% topline growth over the next 5 years with a 3.5% EBIT margin in year 5. I would also anticipate 1.5% dilution annually with a 16X EV/EBIT exit multiple at the end of year 5. Unfortunately that only works out to a ~5% expected return, which is far below what the market has done historically. In fairness I’m being conservative with the assumptions, but even still it’s a country mile away from being compelling and likely a name I won’t revisit.

***Disclosure: I have no position in the security mentioned above, nor do I have any plans to purchase within the next 72 hours. This article is intended for educational purposes only and in no way should be interpreted as investment advice