The Buckle, Inc. $BKE

1. Is the company undervalued?

EV/EBIT: 6.64

Price/Sales: 1.70

Price/Book: 4.18

$BKE trades at an absurdly low valuation and is a high-quality business, averaging ~20% operating margins historically. With that said it’s unlikely $BKE puts up the same numbers over the proceeding 12 months, with most analysts forecasting a 10% decline in revenues. Even still, $BKE shareholders could be in for outsized returns if the business re-rates to a sensible multiple. This coupled with $BKE’s strong balance sheet and dividend makes it an interesting idea.

2. Can I easily explain what the company does?

Yes, they are a retailer primarily located in the Mid-West. They sell reasonably priced apparel to a younger demographic.

3. Does the cash flow statement line up with income statement?

Yes, for the most part cashflows have been higher than reported earrings:

Most of their excess cashflow went towards dividends paid out and capital expenditures, which I’m A-okay with.

4. Is the Balance Sheet Healthy?

Total Debt: $291.7M

Total Cash: $415.3M

Current Ratio: 2.38

FORTRESS BALANCE SHEET!!!!

5. How profitable is the business?

Gross Margins: 48.06%

Net Margins: 18.36%

ROIC: 26.92%

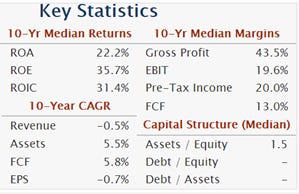

10-yr Revenue CAGR: -0.5%

It’s clear to see that $BKE is a high-quality business, but the trailing data is running a bit hot compared to historical averages:

Notwithstanding, even using normalized metrics $BKE is still well above average in regards to profitability. The one glaring weakness is their declining revenue, which topped out at $1.15B in 2015. $BKE is a potential melting ice cube, which is the likely culprit for their low valuation.

6. Is management rewarding shareholders

$BKE currently offers shareholders a generous 3.38% dividend yield. Unfortunately management hasn’t been repurchasing shares, but they’re certainly not shy about issuing stock based compensation:

This is almost a doubling from last year and I really don’t like when management dilutes shareholders in sneaky ways such as this. Furthermore not buying back shares when your company is trading at a such a low valuation is a strong indication that management is clueless in regards to capital allocation. All in all shareholders are receiving an above average yield, but there’s a lot left to be desired.

7. How does the company stack up against their peers?

$BKE’s most comparable competitor is Dillard’s Inc. $DDS:

$DDS Price/Sales: 0.76

EV/EBIT: 6.69

Gross Margins: 38.31%

$DDS and $BKE trade around the same valuation and both have strong balance sheets. However $BKE is more profitability and has had revenues decline by less compared to $DDS in the last 5 years. For these reasons $BKE offers a better risk/return profile IMO.

8. What’s the counter argument?

By far the biggest counter argument is that $BKE is a melting ice cube and the business is in terminal decline. E-commerce has taken its toll on brick mortar retailers and $BKE is no exception. Moreover $BKE has reduced its store count, which further confirms this thesis.

I’m inclined to buy into this bear arguments, as $BKE’s management hasn’t hinted at any avenues for growth. Furthermore many retailers have been touting their progress in e-commerce as a push back for slowing in store sales. Conversely $BKE doesn’t segment digital sales from in person sales, which leads me to believe that their e-commerce sales suck.

9. Is the company unsexy, uncool, or contrarian?

$BKE has 6 analysts covering the firm with 3 holds, 2 outperforms, and 1 buy rating out. I was honestly stunned to see this level of excitement for a no growth retailer, so for that reason $BKE is more consensus than contrarian. I will say however that $BKE is unsexy and uncool, as it’s a brick and mortar retailer located in mostly fly over states (sorry rust belters, I’m one of those coastal elites).

.

10. Is there something I think the market may be missing?

The most compelling reason to own $BKE is the valuation. Even if earnings fall by 10% their forward EV/EBIT would be 7.31. This in my opinion is too low for a profitable business with strong cashflows. Additionally I’m not so sure analysts are gonna be right about slowing sales. For example $BKE releases monthly shareholder reports and in August sales were up 43% compared to 2020. If this trend persists, $BKE is going to worth a lot more than $1.86B.

Final Thoughts:

Retail is an extremely competitive business, which Warren Buffett has famously advocated to stay away from. Additionally $BKE is showing signs of the prototypical value trap, i.e. it’s melting ice cube. While the business is profitable and probably undervalued at current levels, it’s not a company I would want to own for the long term. This on top of the questionable capital allocation decisions made by management, makes it an easy pass for me.

***Disclosure: I have no position in the security mentioned above, nor do I have any plans to purchase within the next 72 hours. This article is intended for educational purposes only and in no way should be interpreted as investment advice