Snap-on Incorporated $SNA

Snap-on Incorporated $SNA

My Investment Checklist

1. Is the company undervalued?

EV/EBIT: 13.16

Price/Sales: 2.98

Price/Free Cashflow: 11.69

$SNA trades at a hefty discount to the market, while throwing off tons of free cash flow and sporting high margins. With that said revenue growth has been negligible in recent years, which is the likely cause for Snap-on’s undervaluation.

2. Can I easily explain what the company does?

Yes, they manufacture and sells tools ie; wrenches, screwdrivers, power tools, etc…

3. Does the cash flow statement line up with income statement?

Yes, cashflows have been consistently higher than reported earnings.

Most of this excess free cash flow went towards outside acquisitions. Snap-on also allocated towards share repurchases, dividends, and capital expenditures.

4. Is the Balance Sheet Healthy?

Total Debt: $1.51B

Total Cash: $904.2M

Current Ratio: 2.47

$SNA has low debt relative to the size of their business and a solid cash cushion. With that said they’ve issued a significant amount of debt recently:

While this raises eyebrows, $SNA does throw off significant cashflow. Therefore it’s something to keep an eye on, but all in all the balance sheet is healthy.

5. How profitable is the business?

Gross Margins: 50.94%

Net Margins: 16.57%

ROE: 18.94%

10-yr Revenue CAGR: 3.9%

Snap-on is a quality business, which offers noticeably better margins than average. Furthermore these margins have been persistent throughout their history:

$SNA achilles heel is their tepid revenue growth. For example, topline has been nearly flat for the last 5 years. Moreover management hasn’t provided a clear path for growth and it could be argued that their industry is facing secular headwinds with electric vehicles taking market share.

6. Is management rewarding shareholders?

Snap-on gives shareholders a 2.22% dividend and they have a long history of share repurchases. I did find it bizarre that I couldn’t find their current authorization plan on the last 10-k or by doing a google search. However they’ve been pretty consistent with buy backs:

It’s interesting to see share repurchases have begun decelerating, especially given the lack of growth. Be that as it may total shareholder yield is well above average and expected to be that way in the future.

7. How does the company stack up against their peers?

Snap-on’s biggest competitor is Sanely Black & Decker $SWK:

$SWK Price/Sales: 2.02

EV/EBIT: 19.58

Gross Margins: 35.31%

$SWK is more expensive than $SNA, they have worse margins, and return less capital to shareholders. In fairness they’ve been growing slightly faster, but only slightly. This is a no brainer $SNA offers investors a more asymmetric bet.

8. What’s the counter argument?

Snap-on relies on sales reps to recommend products to their customers. This could result in a melting ice cube situation, as customers could eliminate the middle men by sourcing product recommendations online instead. Moreover the need for automotive parts will begin to decrease as more consumers adopt electric vehicles.

I’m not gonna lie these bear points make intuitive sense to me. I personally hate talking to sales people, 99% of them are self-serving and lack ethics. If that statement triggers you, odds are you are one of the self-serving dim wits I speak of. (It’s also important to note that I myself was a sales rep for 5 years out of college). Additionally electric vehicles are going to keep taking market share from ICE vehicles for years to come. Therefore, ancillary industries like tool manufacturers are going to face headwinds, unless they find a way to pivot. The only saving grace is $SNA low valuation, which could imply that all the bad news is already priced into today’s share price.

9. Is the company unsexy, uncool, or contrarian?

I was stunned to see that $SNA has 8 analysts covering the stock with 4 buy ratings and 4 hold ratings out. For this reason, Snap-on cannot be considered contrarian. It’s however certainly unsexy and uncool, unless you hang out with a bunch of gearheads (LOLZ).

10. Is there something I think the market may be missing?

Mr. Market may be overly pessimistic regarding future growth for $SNAP. They recently purchased 3 outside companies. If these acquisitions pan out, it would not be unreasonable to forecast 10% growth. If $SNA can grow investors would be in for outsized gains, as the business is quite profitable.

Final Thoughts:

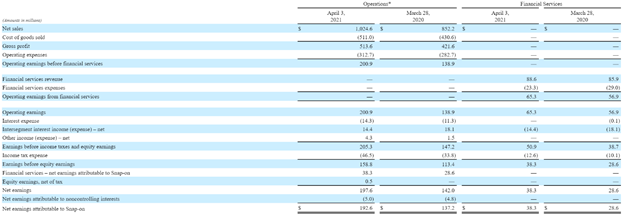

Snap-on is a good business, but I’m unable to trust management. For example they just bought 3 companies; a SaaS business, a “tool control solutions business”, and a tire diagnostic company. Other than the last business, I don’t any synergies with the traditional Snap-on red tool box. It feels like management is doing everything in their power to artificially engineer topline revenue growth. This may make the C-suite look competent for a few quarters, but doesn’t drive long-term shareholder value. Moreover their last 10-k is littered with footnotes and indecipherable lawyer speak. This is a big-time red flag and makes me think there’s some turmoil going on behind the scenes. Finally they way report financial statements is especially peculiar:

I’ve never in my life seen “Earnings before equity earnings”! Also why would they be separating operations and financial services??? It’s not like Snap-on is a bank or insurance company! In summation I don’t care if a business is trading at 2X earnings, if management is doing sketchy things the company is un-investable!

***Disclosure: I have no position in the security mentioned above, nor do I have any plans to purchase within the next 72 hours. This article is intended for educational purposes only and in no way should be interpreted as investment advice.