Penn National Gaming, Inc. $PENN

Penn National Gaming, Inc. $PENN

My Investment Checklist

1. Is the company undervalued?

EV/EBIT: 16.88

Price/Sales: 1.67

Price/Book: 2.96

$PENN trades at a meaningful discount to the market, while offering solid margins and growth potential. The stock recently sold off after a lackluster earnings report and unfavorable news regarding Dave Portnoy’s past personal relationships. Notwithstanding $PENN’s core business remains strong and investors could see outsized returns if management executes on their growth strategy.

2. Can I easily explain what the company does?

Yes, they are a gambling company with casinos located throughout the United States. They also engage in mobile sportsbook betting.

3. Does the cash flow statement line up with income statement?

Yes, cashflows have been consistently higher than reported earnings:

Most of their free cash flow went towards capital expenditures, debt repayment, and outside acquisitions.

$PENN bought LuckyPoint Inc, Hollywood Casino Perryville, and Score Media and Gaming Inc. in the past year. All of these acquisitions appear to have synergies with Penn’s existing business model. The price paid for these businesses however are less than desirable. For example, LuckyPoint was acquired for $12.7M and Hollywood Casino Perryville for $39.4M. Moreover $PENN recognized $8.8M and $9.2M of goodwill for LuckyPoint and Hollywood Casino Perryville respectively. Put differently Penn paid a ~ 34.5% premium for these companies, which is an excellent way to incinerate shareholder value.

There’s no financial information out regarding Score Media and Gaming Inc., as the purchase was executed in October. My suspicion is that this acquisition will add significantly more goodwill to their balance sheet. In fairness there’s a chance these acquisitions pan out and add value, but that bar is incredibly high given the price Penn paid.

4. Is the Balance Sheet Healthy?

Total Debt: $11.6B

Total Cash: $2.73B

Current Ratio: 2.82

$PENN holds a lot of debt relative to their market cap, however over $8.8B of that debt comes from long term lease obligations. This is significantly overstating their debt burden. For instance, Penn is already expensing ~ $156M annually for lease obligations in their cashflow statements. Furthermore $PENN is paying around $193M in net interest payments and the coupon on these bonds are quite reasonable. Considering that $PENN just posted $694M in free cash flow, the debt load is more than manageable. All things consider, Penn actually has an above average balance sheet.

5. How profitable is the business?

Gross Margins: 48.88%

Operating Margins: 17.92%

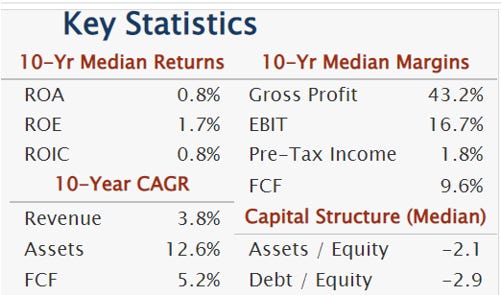

ROIC: 5.7%

10-yr Revenue CAGR: 3.8%

$PENN is objectively above average in regards to profitability and has been fairly consistent with their margins historically (excluding Covid). Conversely their ROIC and ROE metrics aren’t great and a strong indication of poor capital allocation:

Having said that online sports betting is brand new, so perhaps Penn’s recent purchases will turn out to be more effective than acquisitions of yesteryear. Furthermore I would expect growth to improve in the future, as mobile gambling is in its infancy. $Penn is no doubt a beneficiary of this secular tailwind, which should last for years to come.

6. Is management rewarding shareholders?

$Penn does not offer a dividend or repurchase shares. Moreover they were an issuer of equity back in 2020, however this was due to coronavirus and seemingly a one time move. Additionally stock based compensation has almost doubled from last year, but only accounts for 0.3% of their market cap. In short it’s impossible to argue that $PENN is rewarding shareholders, but they’re not really diluting shareholders either. Being that Penn is in a growing industry, it may be more beneficial to fund growth opportunities instead of returning capital back to shareholders.

7. How does the company stack up against their peers?

Penn’s biggest competitors are DraftKings Inc. $DKNG and Caesars Entertainment $CZR:

$DKNG Price/Sales: 12.31 $CZR Price/Sales: 2.35

EV/EBIT: N/A (negative earnings) EV/EBIT: 42.9

Gross Margins: 38.84% Gross Margins: 53.42%

We can easily eliminate $DKNG as they’re selling at an absurd valuation and lighting money on fire quarter after quarter. Side point $DKNG has exceptional growth, but it’s rather easy to spend $1 in order to grow by $0.50 and that’s exactly what they’re doing.

$CZR is a bit more difficult to analyze as their EV/EBIT ratio is overstated. They lost money in Q4 of 2020, if we replace that with 2019 numbers the EV/EBIT would be 28.74 (which is still high). $CZR also offers investors higher margins and have historically grown faster. Having said that the future growth prospects for $PENN may be more attractive. $PENN is the most asymmetry opportunity, as they have the lowest valuation, good margins, and excellent growth prospects.

8. What’s the counter argument?

The counter argument is that mobile gambling will be a winner take all market, as well as the ongoing media circus surrounding Business Insider’s piece on Dave Portnoy.

Anyone with a brain should be able to conclude that the Business Insider article was a calculated hit piece done by a bunch of left-wing lunatics who have ZERO sense of humor. In short, Portnoy had weird sex with two barely legal girls a couple of summers ago. The girls in the article have even come out and said that no sexual assault/abuse happened with them and Portnoy. You can come to your own conclusion about Dave Portnoy, but this is a free country and rich dudes will always want to bang hot chicks. The irony here is quite rich, as the CEO of Business Insider Henry Blodget is a confirmed scumbag (feel free to google search). If someone spent 8 months digging thru Blodget’s past there would be a graveyard of morally reprehensible behavior.

The winner take all argument is actually compelling, as I could see online gambling playing out the same way as ride-sharing apps. Having said Uber and Lyft exist in a duopoly, not a monopoly! Intuitively I would be willing to bet (Lolz) that Penn comes out as a major player. Being that they have a significant marketing advantage and should be able to outlast their money losing competition.

9. Is the company unsexy, uncool, or contrarian?

$PENN has 8 analysts covering the firm with 1 sell, 6 holds, and 1 buy rating out, which doesn’t make them either contrarian or consensus. I would however consider the stock to be cool, as a monkey could tell you they’re in a growing industry and every frat boy in America owns the stock.

10. Is there something I think the market may be missing?

Penn acquired Barstool Sports a few years back, which has arguably been their best acquisition to date. Barstool has a die-hard fan base and candidly I’ve been a fan since 2010, so there’s a good amount of bias in this write-up.

With that said, Barstool allows $PENN to market in a unique and extremely low-cost way. Barstool has engaging personalities that resonate with sports fans in a way no other competitor can replicate:

This is a massive competitive advantage which I can’t quantify, but at the same time isn’t showing up in any financial metric.

Final Thoughts:

$PENN is an interesting investment idea given the recent selloff and future growth prospects. Having said that, it’s not a wonderful business and is only kind of cheap at current levels. If Penn becomes the biggest player in online gambling, it’s a steal at the present valuation. However I’m not so sure that will happen and margins could erode as they compete for market share. Additionally shareholders aren’t being compensated to wait and I believe their recent acquisitions will lead to future write-offs. Nonetheless it’s a stock I’ll continue to watch, as there’s big upside potential. If management executes and takes a more shareholder friendly approach I may re-visit.

***Disclosure: I have no position in the security mentioned above, nor do I have any plans to purchase within the next 72 hours. This article is intended for educational purposes only and in no way should be interpreted as investment advice