Nathan’s Famous, Inc. $NATH

Nathan’s Famous, Inc. $NATH

My Investment Checklist

1. Is the company undervalued?

EV/EBIT: 12.78

Price/Sales: 3.21

Price/Cash Flow: 23.43

$NATH trades at a meaningful discount to the market. They’re a high-quality business which has grown slowly historically. Moreover $NATH faces easy comps over the next few quarters, which makes it an interesting investment idea.

2. Can I easily explain what the company does?

Yes, they manufacture and sell their iconic hotdogs and other food related products. Most of their revenue comes from selling product directly to Nathan’s franchises, as well as licensing agreements with third party vendors.

3. Does the cash flow statement line up with income statement?

The cashflow statement does not line up over the last 7 quarters. Furthermore it hasn’t really lined up since 2018, which is obviously quite disconcerting.

Most of last year’s free cash flow went towards dividends paid out and capital expenditures.

4. Is the Balance Sheet Healthy?

Total Debt: $156M

Total Cash: $79.5M

Current Ratio: 6.57

$NATH does hold a decent amount of debt relative to their market cap. However they do have a large cash cushion and an exceptional current ratio. With that said they’re paying over $10M annually in net interest. The coupons on these bonds are in the ~6.5% range, so the bond market is certainly implying some risk. Moreover $NATH hasn’t ever posted more than $28M in operating income annually, meaning that there’s not a lot of meat left on the bone for equity owners. For this reason, Nathan’s get a barely passing C- in regards to balance sheet health.

5. How profitable is the business?

Gross Margins: 46.86%

Net Margins: 14.35%

ROIC: 23.46%

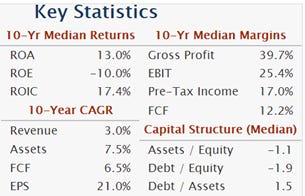

10-yr Revenue CAGR: 3%

Nathan’s had an unusually bad trailing 12 months, due to coronavirus and restaurants/venues being closed down. With that said their profitability metrics didn’t suffer and actually improved compared to historical averages:

Even if we assume some mean reversion for margins, $NATH is still an above average business. However Nathan’s revenues have been declining ever since 2018 when sales topped out at $104M. Be that as it may sales are expected to be up massively YOY, so perhaps the trailing data is painting an overly pessimistic picture.

6. Is management rewarding shareholders?

$NATH offers a 2.04% dividend and has a share repurchase plan in place. It’s important to note however that Nathan’s hasn’t repurchased any shares since the quarter ending in 06/2020. I don’t fault them for halting buybacks due to business uncertainly, but share repurchases have been rather weak historically. Notwithstanding $NATH hasn’t diluted shareholders and are currently offering an above average yield.

7. How does the company stack up against their peers?

The most comparable company I found for $NATH was Dine Brands Global, Inc. $DIN. Their most notable brands are IHOP and Applebee’s.

$DIN Price/Sales: 1.59

EV/EBIT: 20.64

Gross Margins: 39.28%

Between the two, valuation and profitability are nearly a wash. $DIN however appears to be a business in secular decline, whereas $NATH is growing slowly. This coupled with $NATH’s better return of capital to shareholders and improved balance sheet, makes it a much better risk/reward IMO.

8. What’s the counter argument?

The biggest counter argument is that Nathan’s business is in secular decline and their balance sheet is worrisome.

Growth is giant question mark for $NATH. Revenues will inevitably increase over the next 12 months, but they’ll have to keep growing after that to delivery satisfactory investment returns. I’m inclined to think that slow growth will happen, as Nathan’s is an iconic brand and the hotdog industry hasn’t been disrupted for over 100 years. Moreover Nathan’s has many levers to pull for growth, they can open up new franchises, sell different products ie; fruit drinks, expand internationally, or start selling some sweet merch (their logo is fire). Furthermore Nathan’s is only a $287M company and doesn’t exactly have a high bar to clear for future growth.

The balance sheet is most likely $NATH’s biggest question mark. Their interest coverage ratio is 2.69, which is frankly horrendous. However this ratio is being fudged by the TTM operating income denominator. If we normalize earnings, I would expect this ratio climb above 3. Furthermore $NATH does have cash on hand to retire some debt early, meaning that annual net interest expenses will likely be lower in the future.

9. Is the company unsexy, uncool, or contrarian?

Nathan’s has 4 analysts covering the stock with 1 sell, 2 holds, and 1 buy rating out. Additionally it’s very in vogue to hate America currently so yes, $NATH is unsexy, uncool, and contrarian.

10. Is there something I think the market may be missing?

As mentioned previously earnings are expected to soar in the coming year. However the current valuation is lower than their historical averages. If we assume a 30% operating margin on revenues of $100M, that would imply a forward EV/EBIT of 12. Moreover Nathan’s just post $10.7M in operating income for the last quarter alone! This feels too cheap for a high quality business with some growth potential. I personally think a fair value would be an EV/EBIT of 15-18, with the caveat being I do anticipate growth.

Final Thoughts:

Nathan’s is an interesting investment idea, but it doesn’t smack me across the face as a no brainer. Shareholders are only receiving a ~ 3% yield and I’m very uncertain about future growth. It wouldn’t shock me if they grew by 5-10% per year for the next 5 years, but revenue declines are also a very possible outcome. For that reason investors would need a multiple re-rating in order to achieve double digit returns. With that said I’m definitely going to park on my watch list, with the hopes that $NATH’s pays down debt in the near term. I’ve often found that Mr. Market doesn’t reward businesses for debt repayment. If this scenario plays out and $NATH is trading around an EV/EBIT of 10 I would be quite interested.

***Disclosure: I have no position in the security mentioned above, nor do I have any plans to purchase within the next 72 hours. This article is intended for educational purposes only and in no way should be interpreted as investment advice