Molson Coors Beverage Company $TAP

Molson Coors Beverage Company $TAP

My Investment Checklist

1. Is the company undervalued?

EV/EBIT: 10.3

Price/Sales: 1.02

Price/Book: 0.77

$TAP is a high-quality business which trades at a large discount to the market. Since 2016 however; revenues, market share, and the stock price have declined. Notwithstanding $TAP is guiding for topline growth in the coming year. If this trend persists, the stock could be severely undervalued at current levels.

2. Can I easily explain what the company does?

Yes, they manufacture and sell beer. Their most notable brands are Coors Lite, Miller Lite, and Blue Moon.

3. Does the cash flow statement line up with income statement?

Yes, cashflows have more or less been higher than reported earnings:

Most of their excess cashflow went towards debt repayment, capital expenditures, and dividends paid out. There’s nothing out of the ordinary here and boring is good in my book!

4. Is the Balance Sheet Healthy?

Total Cash: $616.3M

Total Debt: $7.52B

Current Ratio: 0.77

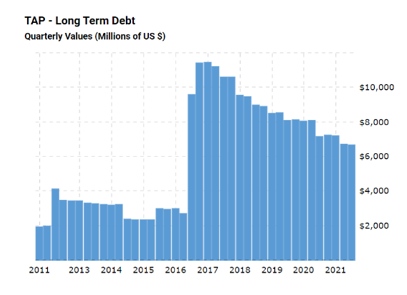

Molson holds a significant amount to debt relative to their market cap. Although, they’ve done a good job of paying it down in recent years:

Furthermore management is guiding for $270M in net interest payments next year. Considering that $TAP just posted ~$1B in free cash flow, the debt burden doesn’t seem so bad. With that said Molson still has a below average balance sheet, but an improving one!

5. How profitable is the business?

Gross Margins: 41.1%

Operating Margins: 16.1%

Net Margins: (4.5%)

Molson’s trailing data is a little wonky due to their acquisition of SABMiller in 2016 and a $1.6B write off in Q4 of last year. Nevertheless $TAP appears to have pricing power as evidenced by consistently above average margins.

Unfortunately revenues have been on a steady decline since 2017, which is by far the biggest question mark for this stock. $TAP just posted 2.5% revenue growth last quarter and is guiding for mid-single digit growth next year. This is extremely promising and potentially signaling a cyclical bottom for earnings.

6. Is management rewarding shareholders?

$TAP reinstated their dividend in July of this year and they currently offer a 1.49% yield. However Molson doesn’t have a share repurchase plan in place and haven’t historically done buybacks either.

I’m actually impressed by management having the stones to halt their dividend during the peak of coronavirus. That was objectively the right move considering the size of the debt burden. Howeva (Stephen A. Smith voice) buying back shares makes way more sense than paying out a dividend. Chiefly because $TAP is trading at a multi-decade low and expected to grow in the future. Buybacks would return capital to shareholders in the most tax efficient way and $TAP’s multiple is more likely than not to expand from here IMO.

7. How does the company stack up against their peers?

Molson’s most comparable competitor is The Boston Beer Company $SAM:

$SAM Price/Sales: 2.85

EV/EBIT: 34.05 (this is overstated)

Gross Margins: 42.12%

$SAM had a negative quarter of earnings last year, if we replace that with 2020 numbers their EV/EBIT would be 19.66. Which still leaves $SAM as the more expensive company. Although $SAM has historically posted slightly better margins and has zero debt. Conversely $TAP offers a dividend, while $SAM has none and is typically a net issuer of equity. Moreover $TAP had positive operating earnings last quarter, while $SAM lost money during the same time. This is a pretty big red flag and makes $TAP the more attractive investment.

8. What’s the counter argument?

The counter argument is that there’s been a structural shift in consumer preferences for beer. Hard Seltzers have been taking increasingly more market share each year for some time now.

It’s hard to argue that seltzers aren’t becoming more popular. If you’ve been in any liquor store recently, you’ve probably noticed they’re taking up more than half the beer case real estate. With that said I’m actually dismissive of hard seltzers having longevity. Consumer preferences shift all the time, for example craft beers were the new rage 10 years ago and now no one cares about them. It’s my belief that the same will happen with hard seltzers, I mean honestly if I go one more summer hearing “ain’t no laws when you drinking claws” I might blow my brains out.

9. Is the company unsexy, uncool, or contrarian?

$TAP has 7 analysts covering the stock with; 1 sell, 5 holds, and 1 buy rating out. Additionally this a stock you wouldn’t be embarrassed to tell your friends you own. For these reasons $TAP is neither unsexy, uncool, or contrarian.

10. Is there something I think the market may be missing?

As mentioned previously $TAP may be at a cyclical bottom for earnings. At the current valuation, Mr. Market must be implying little to no growth for Molson. This coupled with a potential slowing of seltzer sales, could result in a massive surprise to the upside for $TAP.

Final Thoughts:

Molson is an interesting investment idea for value investors who believe in mean reversion. However it’s not compelling enough for me to buy, as investors would need a multiple re-rate in order to achieve above market returns. While revenues are expected to grow, management is guiding for flat earnings next year. In fairness $TAP has traded around a 20X EV/EBIT historically, which would be roughly a double from here. Nonetheless I’m not sure $TAP deserves that multiple unless they start growing earnings by 6% or so per year. Although it’s a company worth tracking, if the balance sheet improves and earnings grow I’ll revisit the idea.

***Disclosure: I have no position in the security mentioned above, nor do I have any plans to purchase within the next 72 hours. This article is intended for educational purposes only and in no way should be interpreted as investment advice