Match Group, Inc. $MTCH

My Investment Checklist

1. Is the company undervalued?

EV/EBIT: 24.6

EV/Sales: 5.06

$MTCH doesn’t appear cheap at surface level, however the company is underearning due to a large non-cash impairment charge. Furthermore $MTCH is incredibly profitable due to their asset light model. Moreover management believes they can grow revenues at mid to high teens in the not so distant future. Throw in the fact that $MTCH is now returning capital back to shareholders, makes this a compelling investment idea.

2. Can I easily explain what the company does?

Yes, they offer dating service apps. Their most notable brands are Tinder and Hinge.

3. Does the cash flow statement line up with income statement?

Yes, cash from operations has been consistently higher than reported income:

Most of their excess cash went towards share repurchases, debt repayment, capital expenditures, and acquisitions. The buybacks are definitely a questionable use of cash as the company was trading at $73/share (~8X EV/Sales) during the time of repurchase. Although it’s difficult to come up with an intrinsic value for $MTCH as management is promising healthy growth ahead. It could turn out to be that $73/share was in fact too low a price, but only time will tell.

Additionally mergers and acquisitions are a large part of Match’s business model. Their most recent purchase was The League dating app in July of this year. Unfortunately I found next to no data regarding The League’s financial metrics. That in and of itself is a bit of a red flag and $MTCH hasn’t been all that successful with any of their latest acquisitions. For example they took a $229M impairment charge on their Hyperconnect acquisition in the most recent quarter. With that said management is showing some self-awareness and hinting at a more disciplined approach to M&A:

Gary Swidler (CFO)

“By contrast, when you look at the acquisition that we made outside of dating, it hasn't gone the way we would have hoped. We are working on it. We think the team is still fantastic. There's more we can do with that business. But there's no denying that, that acquisition of Hyperconnect has not worked out the way we had hoped, at least in the first year. And so the bar has been raised around non-dating acquisitions. That's not to say that we wouldn't do them. But we need to be more convinced in both the growth that can be derived from those kinds of acquisitions as well as the profitability levels. And we need to see a clear path to profitability, if not immediate profitability. So I think the standards will be higher for an acquisition outside of dating.”

Nevertheless I’m a bit skeptical regarding management’s ability to allocate capital in way that would drive shareholder value.

4. Is the Balance Sheet Healthy?

Total Debt: $3.83B

Total Cash: $472.9M

Current Ratio: 1.28

$MTCH holds some debt relative to their market cap and have interest payment hovering at $137M annually. Even with compressed earnings the company still has a 4.75X net interest coverage ratio, which is well above average. This gives Match a good, but not great balance sheet grade.

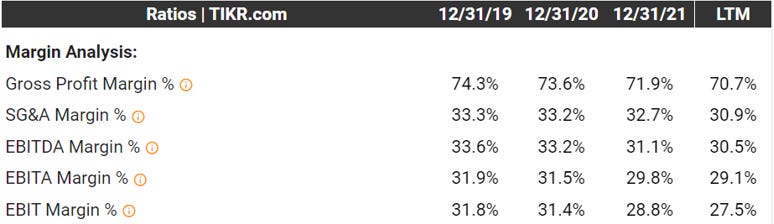

5. How profitable is the business?

Gross Margins: 70.7%

Operating Margins: 27.5%

Net Margins: 3.5%

Being a software company it should come as no surprise that $MTCH sports a high margin profile. In fact, it could be argued that these numbers are understated:

Moreover the adjusted operating margin last quarter was 36%. Assuming the company has no additional one-off charges, I don’t think it would be unreasonable to forecast 30ish% operating margins moving forward.

6. What is the company’s growth potential?

$MTCH spun off from their parent company $IAC a little over two years ago, so the backwards looking data is super wonky. Notwithstanding the core business has grown at roughly mid-teens during its brief history. Furthermore $MTCH was able to grow topline at 12% YOY in a challenging Q2. The CFO made the following comments regarding future growth:

Gary Swidler (CFO)

“Sure. Let me jump in and take that, and thanks for the question. And as I talked about a little bit with the answer to John's question as well about 2023, so I'll try to weave that together. First of all, I want to say off the bat, we remain confident that this business can return to mid- to high-teens revenue growth. There's a lot of opportunity for us, and it really comes down to execution. And right now, we didn't execute as we needed to and as we expected to in the first part of the year. So we need a few quarters to rebuild the momentum in the business. And as BK has talked about extensively, in particular, we need a few quarters to get the Tinder team to improve their overall execution and deliver on their product road map.”

I honestly have no clue how big a TAM there is in the dating services world. However I do know that trees don’t grow to the sky and 15% growth will almost certainly not last forever. With that said, there’s no doubt some runway left here, particularly in international markets. I’m a value guy at heart, so I would be apprehensive to underwrite any more than 10% sales growth over the next 3-5 years.

7. Is management rewarding shareholders?

Match does not offer dividend, however they are authorized to buyback 9.3M shares outstanding currently. Being that the stock is down ~40% from the level of their recent repurchases, it would makes sense for management to double down here. Additionally the company does generate significant operating cashflow, around $900M per year so there’s plenty of dry powder. With that said $MTCH does a fair amount of acquisitions and issued $171M in stock based comp last year. All in all I wouldn’t expect any more than $200M returned to shareholders on net, which only works out to a 1.6% net shareholder yield.

8. How does the company stack up against their peers?

The closest competitor to $MTCH is Bumble $BMBL:

$BMBL EV/Sales: 4.67

EV/EBIT: 451.2

Gross Margins: 72.5%

$BMBL is slightly cheaper relative to sales and have grown at a faster clip in the last two years. However the company is barely generating any profit and issuing an absurd amount of stock based compensation. It could turn out that Bumble’s business model is about to inflect profitably, but there’s way more uncertainty there. Personally speaking $MTCH seems like a better risk adjusted bet, but $BMBL likely offers higher upside potential.

9. What’s the counter argument?

The counter argument is that the dating app industry is ridiculous competitive with effectively zero barriers to entry. Old school investors would argue that incumbents will relentlessly fight for market share and shrink profit margins for everyone along the way.

I don’t have a strong view on the future of dating apps, so my default would be assuming this age-old tale plays out. I wouldn’t be surprised if some teenager tinkering in his basement comes out with the latest and greatest dating app a few years from now. Candidly this is all speculation on my end, but I don’t see any meaningful differentiator amongst Match’s portfolio of apps.

10. Is there something I think the market may be missing?

I just said that $MTCH has basically no competitive advantage, although there’s a decent chance the dating app industry turns into a winner take all market. This thesis has played out with a few large tech companies, Google probably being the best example of this. It should go without saying that I’m not comparing Match Group to Google, but $MTCH is no doubt the #1 player in the space right now. When you think of dating apps you think of Tinder and that’s already deeply rooted into pop culture. For example, there’s no Netflix special titled the Bumble Bandit (if they steal this idea I’m suing)!

Final Thoughts:

I walked into this write-up knowing that I wouldn’t seriously entertain buying the stock. Frankly it’s outside my circle of competence and software companies scare me to death. With that said I can see the appeal if you’re of the mindset that $MTCH can grow low teens and return some capital back via share repurchases. In closing it’s a pass, but I enjoyed learning about the company and maybe some day in the future this knowledge will pay off.

***Disclosure: I have no position in the security mentioned above, nor do I have any plans to purchase within the next 72 hours. This article is intended for educational purposes only and in no way should be interpreted as investment advice