Levi Strauss & Co. $LEVI

Levi Strauss & Co. $LEVI

My Investment Checklist

1. Is the company undervalued?

EV/EBIT: 10.17

EV/Sales: 1.3

Price/Book: 3.74

$LEVI is a durable brand, which is trading at an attractive price. The company is also forecasting high single digit revenue growth and returning 60% of free cash flow back to shareholders. If management can hit their goals, the stock is likely selling at a steep discount.

2. Can I easily explain what the company does?

Yes, they’re an apparel manufacturer with most of their revenue coming from Levi’s jeans. They also own the brands; Dockers and Beyond Yoga.

3. Does the cash flow statement line up with income statement?

Yes cashflows have been consistently higher than reported earnings:

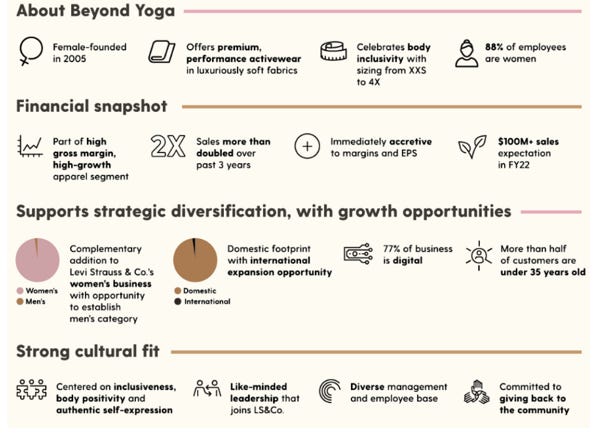

Most of their excess cash went towards debt repayment, acquisition costs, share buybacks, capital expenditures, and dividends paid out. The obvious question mark is the purchase of Beyond Yoga for ~$391M.

Beyond Yoga is an activewear company, who targets a larger female customer (credit to me for not being mean). Beyond Yoga is expected to do $100M in sales in 2022 and grew at ~26% YOY for the past 3 years. What strikes me as odd is that $LEVI bought the company at 4X forward sales, when their stock for was trading for 2X sales. That’s a massive valuation discrepancy, especially considering their core business is growing at a market rate. Moreover the presser they released reeks of ESG/Woke BS:

No offense, but I couldn’t give a fuck less about an 88% female workforce or their “strong cultural fit”. Furthermore growth is bound to decelerate and I would be stunned if this acquisition doesn’t result in a future write down. Not off to a hot start!

4. Is the Balance Sheet Healthy?

Total Cash: $777.15M

Total Debt: $2.22B

Current Ratio: 1.55

$LEVI does hold some debt, but $953M of which is in operating leases. Additionally interest expenses only came in at $53M last year, which is over 14.5X coverage. For these reasons the balance sheet is exceptionally strong.

5. How profitable is the business?

Gross Margins: 58.35%

Operating Margins: 12.725

Net Margins: 10.03%

As you can see $LEVI is certainly an above average business. This reflects a durable brand, which customers are willing to pay a premium for. With that said, trailing margins are above historical averages. However management thinks they can hit 15% EBIT margins by 2027. They hope to accomplish this by reducing costs and offering a higher margin product mix.

Frankly I’m a bit skeptical this happens, for starters inflation remains white hot. On top of this, Levi’s is planning to grow their direct to consumer business rapidly. The DTC strategy is by nature lower margin, so I’m really not understanding how margins will expand under this model.

6. What is the company’s growth potential?

7-yr Revenue CAGR: 2.79%

7-yr Operating Profit CAGR: 6.79%

7-yr FCF CAGR: 20.28%

As you can see the bottom line has grown faster than top line. Additionally most of this growth has been organic, which is good to see. Management is also guiding for 6-8% revenue growth over the next 5 years. I actually don’t think this forecast is unreasonable as Levi’s has plenty of room to expand thru e-commerce and internationally. On the other hand, investors shouldn’t expect earth scattering growth moving forward.

7. Is management rewarding shareholders?

Levi’s is offering shareholders a 2.34% dividend and just approved a $750M share repurchase program. Management stated that they plan on returning ~60% of FCF back to shareholders annually. $LEVI posted $550M in free cash flow last year and issued $67M in stock based compensation. Therefore we can assume $265M going back to investors in the next 12 months. This works out to 4.1% net shareholder yield, which is solid but not otherworldly.

8. How does the company stack up against their peers?

Levi’s closest competitor is American Eagle Outfitters, Inc. $AEO:

$AEO EV/Sales: 0.73

EV/EBIT: 7.08

Operating Margins: 10.03%

While $AEO is cheaper and returning more cash back to shareholders, their business is of much lower quality. American Eagle is a no growth business, with thin margins and zero brand loyalty. Moreover the valuation discrepancy isn’t massive, so there’s no reason to buy $AEO over $LEVI.

9. What’s the counter argument?

The counter argument is that growth will come in slower than expected and margins will fail to expand.

I partially buy into this bear thesis, frankly I think 15% operating margins are a pipe dream. For example that’s over 50% higher than their long run average of 9.8%. On the other hand, 6-8% revenue growth seems attainable as there’s white space to move into more retail locations and expand their DTC business. So, all in all a mixed bag here.

10. Is there something I think the market may be missing?

Given the current valuation, Mr. Market is pricing in low growth for $LEVI. I don’t think that’s gonna be the case and would argue $LEVI should if anything have a slightly premium valuation. The company is growing at a market rate, but has above average profitability and returns meaningful capital back to shareholders. That to me deserves at least a 15X multiple!

Final Thoughts:

My base case would be as follows revenues growing 6% per year, a 4% total shareholder yield annually, a 15X EV/EBIT exit multiple, and 12% EBIT margins by 2027. That works out to a ~17% expected return per year, which is pretty good. Unfortunately most of that return is coming from multiple expansion. Additionally I don’t like the vibes I’m getting from management, chiefly because I think they’re overpromising investors. This coupled with an openness to grow via acquisition is usually something I steer clear of. So, for these reasons it’s a pass and something I likely won’t revisit.

***Disclosure: I have no position in the security mentioned above, nor do I have any plans to purchase within the next 72 hours. This article is intended for educational purposes only and in no way should be interpreted as investment advice