Las Vegas Sands Corp. $LVS

Las Vegas Sands Corp. $LVS

My Investment Checklist

1. Is the company undervalued?

Price/Book: 10.72

Forward EV/EBITDA: 17.43

Forward EV/Sales: 5.19

$LVS is priced at an Enterprise value of $41.46B, which is the cheapest it’s been since 2015. Furthermore Las Vegas Sands has historically been tremendously profitable, averaging 25%+ operating margins over the last decade. Moreover $LVS has exhibited revenue growth, while returning meaningful capital back to shareholders. Unfortunately most of their business is done in Macao and Singapore, which is under the purview of China’s authoritarian control. There’s significant uncertainty surrounding Macao’s stance on re-opening their economy as well as renewing gambling licenses with Las Vegas Sands. However if things go back to normal, $LVS investors could be in for outsized returns.

2. Can I easily explain what the company does?

Yes, they own in operate casinos and resorts in Macao, Singapore, and Las Vegas. Most of their revenue stems from casino, mall, and hotel operations.

3. Does the cash flow statement line up with income statement?

Yes, for the most part cashflows have been consistently higher than reported income:

$LVS lost money last year due to Covid-19 shutdowns and for that reason their only meaningful expense was capital expenditures.

4. Is the Balance Sheet Healthy?

Total Debt: $14.45B

Total Cash: $2.06B

Current Ratio: 2.19

$LVS does hold a sizeable chunk of debt relative to their market cap and was forced to take on more debt as a result of coronavirus. However their debt situation isn’t egregious, paying an average interest rate of 4.4% on $632M of annual interest expenses:

For a company who hasn’t earned a profit in 7 quarters, I would’ve expected bond investors to demand a higher rate. Notwithstanding if we assume next year’s operating income is 50% of 2019 ($3.8B), then $LVS net interest coverage ratio is over 3. This of course is not good, but a far cry from a business about to file chapter 11.

5. How profitable is the business?

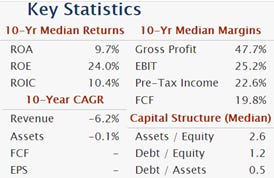

The trailing data is useless, so here’s a look at what $LVS did over the last 10 years:

It’s clear to see that $LVS is extremely high-quality business during normal times. The only thing you can nitpick is their mediocre revenue growth, which was a ~5% CAGR from 2011-2019. Be that as it may, this number is only slightly below average whereas everything else is well above average. All in all, Las Vegas Sands gets high marks in regards to profitability.

6. Is management rewarding shareholders?

$LVS hasn’t paid a dividend since March of 2020 or repurchased any shares since 2019. This was a prudent capital allocation decision by management, as they’re still losing money. Looking past the current turmoil, management returned around $3.8B annually to shareholders from 2017-2019. That would equate to a mind-blowing 13.25% shareholder yield at current levels. It’s incredibly unlikely $LVS matches those numbers in the next two years, but if the business stabilizes I would expect management to start hammering share buybacks.

7. How does the company stack up against their peers?

$LVS’s major competitors are Wynn ($Wynn) and MGM ($MGM)

$WYNN Forward EV/Sales: 3.84 $MGM Forward EV/Sales: 3.64

Forward EV/EBITDA: 15.68 Forward EV/EBITDA: 14.52

10-yr Average EBIT Margin: 18.3% 10-yr Average EBIT Margin: 11.6%

$LVS trades at a slight premium to $WYNN and $MGM, however it’s by far the most profitable out of the 3. Moreover they’ve all grown around the same rate and been generous returning capital back to shareholders. With that said the most critical determinate is balance sheet health as casino stocks have been bleeding red ink for almost 2 years now. $LVS without question has the best balance sheet and for that reason I believe they offer investors the best risk/reward.

8. What’s the counter argument?

The Chinese government is certainly the biggest threat for $LVS. They seem disgruntled that US businesses are operating a majority of the casinos located in Macao and are threating to increase regulations on gambling licenses. Reading in between the lines it appears that China wants more domestic and less American companies in Macao. Furthermore Macao is reopening their economy at a snails pace compared to the rest of the world. For example Las Vegas Sands’ Macao hotel occupancy is only at ~ 50% compared to 85.5% in the US, as of their last quarter.

These are all excellent arguments, to which I have no retort. I have no idea what the regulators are gonna do or when/if Macao gets back to pre-pandemic levels. What I will say is that these risks are likely already being discounted into today’s share price. Most investors are unwilling to invest in China and a business siphoning off cash, which is exactly why the stock could be mispriced.

9. Is the company unsexy, uncool, or contrarian?

$LVS has 8 analysts covering the stock with 3 sells and 5 hold ratings out. It should come as no surprised that these candy ass ivy league yuppies wouldn’t be bullish on a stock like $LVS. Additionally $LVS is certainly unsexy and uncool as anything China related is uninvestable according to the know it alls on Fintwit.

10. Is there something I think the market may be missing?

Mr. Market has been indiscriminately selling off Chinese equities regardless of the reason. For example, Alibaba and Tencent recently sold off on the Evergrande debt crisis news and due to regulation regarding the education sector. For all intents and purposes both of the aforementioned businesses have nothing to do with education or real estate, but they’re located in China. So to answer the question I don’t think Mr. Market is missing anything, but rather overacting to the fluid situation.

Final Thoughts:

Analysts are forecasting $2.35B in operating income over the next 12 months for $LVS, but I think this number could be much higher. For example $LVS just posted positive operating cashflows of $83M last quarter. While that number is piss poor, they’ve been trending in the right direction for the last few quarters. Additionally I have a hard time believing there’s more than a 6 month shelf life on coronavirus restrictions. After the winter of 2022’, I anticipate demand being thru the roof and a record setting year for 2023. I think $4b in operating income for 23’ is a reasonable estimate, which would equate to 2023 forward EV/EBIT of 10.36. This is cheap for a company which has traditionally traded around an EV/EBIT of 15-20, but isn’t ridiculously cheap. Moreover if we extrapolate out the last quarter of earnings $LVS is burning thru $1.14B in cash per year, which makes the forward enterprise value prediction quite murky. I would want at a minimum to double my money for investing in a risky name like $LVS. In order to do so, I would need $LVS to outperform my fairly bullish assumptions and have the multiple re-rate towards the higher end of where it’s been historically. This of course is unlikely, but I will keep watching $LVS as the indiscriminate selling could persist or the business could start performing above expectations.

***Disclosure: I have no position in the security mentioned above, nor do I have any plans to purchase within the next 72 hours. This article is intended for educational purposes only and in no way should be interpreted as investment advice