Foot Locker, Inc. $FL

My Investment Checklist

1. Is the company undervalued?

EV/EBIT: 5.26

Price/Sales: 0.53

Price/Book: 1.33

Foot Locker is a decent quality business, which trades at a ridiculously low multiple and returns a significant amount of cash back to shareholders. With that said Foot Locker’s growth prospects are bleak at best. Herein lies the crux of $FL as an investment opportunity; is the business a melting ice cube or can they keep growing modestly?

2. Can I easily explain what the company does?

Yes, they’re a retailer who sell sneakers and apparel. Their most notable brands are Footlocker, Champs, and Eastbay.

3. Does the cash flow statement line up with income statement?

Yes, cashflows while choppy have been higher than reported earnings:

Foot Locker’s biggest expense this year has been the acquisitions of WSS and Atmos for $737M and ~$360M respectively. I’ve never heard of either company, but there does appear to be some synergies as both are sneaker resellers located on the West Coast and Japan. $FL is guiding for both businesses to grow at low double digits, with low-mid teen EBITDA margins, and add $0.44- $0.48 in EPS for 2022. On its face that seems pretty good for a business that’s desperate to growth, however the price $FL paid makes no sense IMO.

If you assume 10% net margins on both businesses, then we can forecast ~$461.7M in added revenues. In other word $FL paid 2.37X sales for outside acquisitions that have virtually the same margin profile as their core business. Furthermore $FL can buy their stock on the open market today for 0.53X sales, which is ~ 4.5X cheaper!!!! In fairness WSS and Atmos are expected to grow double digits, but that growth is unlikely to make up for the premium being paid. Moreover $FL has a history of taking impairment charges:

Candidly these outside purchases reek of management looking to artificially create growth at the detriment of shareholders.

4. Is the Balance Sheet Healthy?

Total Debt: $3.56B

Total Cash: $1.34B

Current Ratio: 1.65

$FL does hold a sizeable amount of debt relative to their market cap. However they only paid ~$12M in net interest payments last year. Even if that number doubles, $FL is throwing off significant free cash flow ($900M last year) so it’s safe to assume they should be able to service the debt. All in all, I would give $FL a solid B in regards to balance sheet health.

5. How profitable is the business?

Gross Margins: 34.42%

Operating Margins: 12%

Net Margins: 10.37%

ROIC: 14.43%

The trailing data is slightly overstating Foot Locker’s historic profitability, but only by a small margin:

$FL is not even close to a wonderful a business, but they’re pretty solid and I would consider them to be a touch below average.

6. What is the company’s growth potential?

10-yr Revenue CAGR: 4.1%

10-yr EBIT CAGR: 4.79%

10-yr FCF CAGR: 14.7%

I was quite surprised to see these numbers from $FL. Intuitively I would’ve thought a mall-based retailer would’ve seen revenue declines over the last decade, a la Abercrombie and Fitch or Build-a-Bear. Considering the present valuation, low single digit growth moving forward would be a massive win for shareholders.

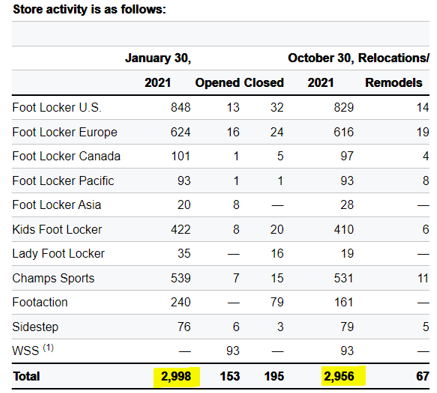

In fact most analysts are forecasting earnings to decline by 1.6% per year going out until 2026. That’s not what you want to hear as an investor and $FL appears to be on net closing down stores:

Nonetheless store closures could benefit long term-profitability. Moreover investing is a game of handicapping and investors could achieve above market returns even in a declining business.

7. Is management rewarding shareholders?

Footlocker currently offers investors a 2.78% dividend and have $660M left on their share repurchase program. $FL has actually been fairly aggressive with their buybacks, averaging ~$325M in repurchases over the last six years. Although considering that $FL raised debt to partially fund $1B in acquisitions, it’s likely that number goes down in the future. With that said I don’t think it’s unreasonable to expect $200M per year in share repurchases for the next few years. This would equate to a total shareholder yield of 7.26% (4.48% from buybacks), which is of course exceptional!

8. How does the company stack up against their peers?

There are no publicly traded shoe resellers, so I’m gonna be lazy and skip this question. (Also don’t bitch, I do this shit for free)

9. What’s the counter argument?

The counter argument is that Foot Locker is melting ice cube city and it’s trading at a low multiple for a reason.

Candidly I think $FL has an incredible fragile business model. For instance if Nike and/or Adidas decided to pursue direct to consumer marketing, then Foot Locker would be totally screwed. With that said, direct to consumer isn’t a new idea and the major sneaker manufacturers would’ve likely pivoted by now if they felt that was best for business. Moreover, using history as a proxy $FL is more likely than not to grow at low single digits.

10. Is there something I think the market may be missing?

I think Mr. Market may be incorrectly assuming negative grow for $FL. This is a name that makes you want to throw up, it’s a brick-and-mortar retailer in a no growth industry with zero moat. It’s likely that analysts covering the stock are being overly conservative. For example you seem a lot dumber for forecasting low single digit growth and being wrong, as opposed to forecasting revenue declines and being incorrect. Furthermore with $FL closing down unprofitable stores, they may be able to grow their bottom line while topline remains flattish.

Final Thoughts:

Foot Locker has historically traded in 6-12 EV/EBIT range. My base case would be a 7% shareholder yield, EBIT decline of 1% per year, and an exit multiple of 8X EV/EBIT. If this happens in 3 years, investors would be looking at a ~21% CAGR from current levels. This is pretty mind blowing and illustrates why value stocks have historically outperformed the broader market!

With that said I’m not ready to own $FL in my portfolio for a couple reasons. Chiefly because I don’t like the recent acquisition moves by management, share repurchases would’ve been a much better allocation of capital IMO. Furthermore retail is a brutally competitive industry and there’s a seemingly infinite amount companies that were perceived as good but wound up filing chapter 11. I don’t think Foot locker is a durable business or has any competitive advantage in the marketplace. Although, it’s definitely worth tracking as the expected return is quite juicy here and Mr. Market could be wrong about Foot Locker’s future growth.

***Disclosure: I have no position in the security mentioned above, nor do I have any plans to purchase within the next 72 hours. This article is intended for educational purposes only and in no way should be interpreted as investment advice