Energizer Holdings, Inc. $ENR

Energizer Holdings, Inc. $ENR

My Investment Checklist

1. Is the company undervalued?

EV/EBIT: 13.9

Price/Sales: 0.85

Price/Book: 7.43

$ENR is a solid business, which offers growth potential at an attractive price. This coupled with a shareholder friendly management, makes $ENR an interesting investment idea.

2. Can I easily explain what the company does?

Yes, they sell batteries and auto care products.

3. Does the cash flow statement line up with income statement?

Yes, cashflows have been more or less been higher than reported earnings:

Most of their free cashflow went towards paying down debt, dividends, acquisition costs, and capital expenditures. In last 12 months Energizer bought FDK Indonesia and a North Carolina based company that specializes in formulations for cleaning tasks. I’m okay with FDK Indonesia as they are a battery manufacturer. Conversely the North Carolina acquisition seems suspect, as the description they gave appears to be intentionally vague. This most likely means they don’t want investors to know about it, which is a red flag in my book.

4. Is the Balance Sheet Healthy?

Total Debt: $3.59B

Total Cash: $207.7M

Current Ratio: 1.7

$ENR holds a significant amount of debt relative to their market cap of $2.53B. Moreover their net interest expenses are bothersome at around $175M per year. Having said that management has done a good job of paying off debt in recent years and refinancing long term debt opportunistically. Furthermore the company is guiding for future growth and free cash flow of $225M this year, which gives Energizer some breathing room. All in all I would give $ENR a disappointing C- in regards to balance sheet health.

5. How profitable is the business?

Gross Margins: 38.55%

Operating Margins: 13.58%

9-yr Revenue CAGR: 3.09%

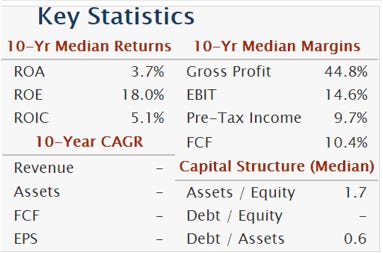

On the surface these numbers look average at best, although margins have historically been better:

While their profitability metrics probably aren’t going to blow your socks off, they’re objectively above average. Furthermore since 2018 $ENR has spent over $2.56B on acquisitions, so it wouldn’t be unreasonable to expect better growth metrics moving forward. For example Energizer is guiding for 8-9% sales growth in the current year.

6. Is management rewarding shareholders?

$ENR is currently yielding a 3.24% dividend and are authorized to purchase up to 7 million outstanding shares. Moreover the company plans on buying $75M worth of stock in Q4 of this year, which would equate to a 2.93% yield!!! That’s outstanding, but unlikely to last forever. I would actually prefer if Energizer cut the dividend and paid off debt instead, as they’re paying close to 5% on outstanding notes. Notwithstanding $ENR shareholders are expected to receive a well above market yield moving forward.

7. How does the company stack up against their peers?

I couldn’t find any publicly traded battery manufacturers and for that reason there’s nothing to compare Energizer to.

8. What’s the counter argument?

The counter argument is that $ENR faces inflationary headwinds and tough competition.

Analysts are getting lazier and lazier by the day, these arguments can be applied to literally every single publicly traded company. There’s no idiosyncratic risk here and no independent thought coming from the analyst community…. Sad!

9. Is the company unsexy, uncool, or contrarian?

$ENR has 7 analysts covering the stock with; 1 sell, 1 under perform, 4 holds, and 1 outperform rating out. Furthermore Energizer passes the, I’m definitely not gonna brag about this stock at a dinner party test. For these reasons $ENR hits the trifecta of unsexy, uncool, and contrarian.

10. Is there something I think the market may be missing?

There seems to be a disconnect between Mr. Market and Energizer’s management team. Management is guiding for high single digit growth and implying the stock is undervalued with their aggressive share repurchase plan. If this trend persists, then $ENR should be trading at a premium and not a discount to the market.

Final Thoughts:

$ENR is an intriguing idea given the business quality, growth potential, and shareholder yield. Unfortunately I don’t think Energizer is growing revenues in a “quality way”. By that I mean they are relying on outside acquisitions for topline growth. Furthermore this is showing up in the data, as gross margins have dropped sequentially since 2018. While I do think that Energizer can keep growing at 8% per year, I’m doubtful that earnings will grow at the same rate. Additionally the balance sheet is in rough shape and management is probably jeopardizing the business long term by being so generous to shareholders short term. For this reason I think $ENR is a pass, but does offer a fat right tail payoff if I’m wrong.

***Disclosure: I have no position in the security mentioned above, nor do I have any plans to purchase within the next 72 hours. This article is intended for educational purposes only and in no way should be interpreted as investment advice