Columbia Sportswear Company $COLM

Columbia Sportswear Company $COLM

My Investment Checklist

1. Is the company undervalued?

Forward EV/EBIT: 17.97

Price/Sales: 2.6

Price/Free Cash Flow: 19.03

Columbia’s trailing twelve-month data is a bit wonky due to Covid. On a forward-looking basis the stock is trading at a discount to the market, while offering solid margins and significant revenue growth. On its face $COLM appears to be an interesting investment idea.

2. Can I easily explain what the company does?

Yes, they manufacture and sell outdoor apparel.

3. Does the cash flow statement line up with income statement?

Yes, for the most part cashflows have been higher than reported earnings:

Most of this excess cash went to paying down debt. $COLM also allocated towards share repurchases, capital expenditures, and dividends. These are all wonderful signs!

4. Is the Balance Sheet Healthy?

Total Debt: $438M.07M

Total Cash: $874.56M

Current Ratio: 3.80

Columbia’s balance sheet is an absolute unit! Fortress balance sheet!!!

5. How profitable is the business?

Gross Margins: 49.77%

Net Margins: 6.4%

10-yr Revenue CAGR: 5.4%

$COLM isn’t the most profitable business, however these numbers are quite serviceable. Additionally the trailing 12 month data is understating how profitable their core business is. For example, Columbia just guided for sales growth of 22% and operating margins of 11.5% in fiscal year 2021. Furthermore gross margins improved to 51.4% in the last quarter, signaling that the turnaround is well underway. Looking past 2021, it would not be unreasonable to assume $COLM’s net margins stabilize around 8% and they continue growing sales at 5-10% per year.

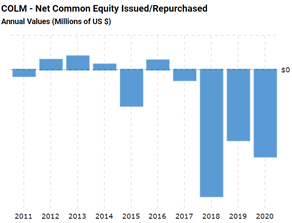

6. Is management rewarding shareholders?

Columbia offers shareholders a 1.02% dividend and they’ve been repurchasing shares at a nice clip recently:

$COLM has $471M left under their current share repurchases authorization, which is ~ 7.08% of their market cap! It’s also worth noting that Columbia suspended their dividend from 3/20- 3/21 due to Covid. Part of me likes the fact that management had the stones to halt their dividend in order to sure up their business. Conversely part of me thinks this was overly cautious as dividends paid out in 2019 only totaled $65M. In fairness it’s unlikely that a Coronavirus situation happens again, so shareholders can expect an above market yield moving forward.

7. How does the company stack up against their peers?

Finding a true apples to apples competitor for $COLM was difficult, being that they operate in a niche outdoor apparel category, however V.F. Corp $VFC is a decent proxy:

$VFC Price/Sales: 3.46

Gross Margins: 52.69%

Forward P/E: 26.71

$VFC offers slightly better margins and a higher dividend than $COLM. However they are much more expensive and were a net issuer of shares in the trailing 12 months. Furthermore $VFC’s direct to consumer strategy is losing sales YOY, while $COLM direct to consumer strategy is growing sales YOY. All in all $COLM gives shareholders a better risk/return IMO.

8. What’s the counter argument?

I couldn’t find a lot of hate for $COLM, however one analyst pointed to Columbia’s low operating/net margins and high valuation as areas of concern.

$COLM doesn’t have great margins but I think this analyst is relying too much on trailing twelve-month data. $COLM is guiding for operating margins of 11.5% next year, which is only slightly below average. Furthermore Columbia has a forward EV/EBIT of ~ 18, whereas the S&P 500 is trading at an EV/EBIT of ~ 26.7. The haters will say I shouldn’t rely on relative valuations, but even on an absolute basis I have a hard time making the case that $COLM is overvalued. In summation there’s really not a lot of bad things you can say about this company.

9. Is the company unsexy, uncool, or contrarian?

Columbia has 8 analysts covering the stock with; 1 sell, 5 holds, 1 outperform, and 1 buy rating out. For this reason the stock isn’t contrarian. However $COLM fails the, could you brag about this stock at a dinner party test. Therefore Columbia is unsexy and uncool.

10. Is there something I think the market may be missing?

Mr. Market seems skeptical of $COLM’s revenue growth and margin improvement. If Columbia hits forward guidance, I would expect to see their multiple to re-rate around a 25 P/E. Moreover I don’t think it’s unreasonable to argue that $COLM can grow around 10% per year for the foreseeable future. Their direct-to-consumer strategy grew at 35% YOY and now makes up 20% of net sales. Direct-to-consumer also benefits $COLM in that those sales are much more profitable. Improved margins and growing revenues tend to be the elixir needed for compounding!

Final Thoughts:

Columbia is an intriguing investment idea and I really like their management team. However even if $COLM hits their 2021 goals, the stock is only slightly undervalued at current levels. I would require a much wider margin of safety given that the company isn’t super high quality or a fast grower. If for whatever reason Columbia gets down to a 14 EV/EBIT I would be very interested. I will say however that the business is definitely worth tracking as it checks every other box with the except of valuation!

***Disclosure: I have no position in the security mentioned above, nor do I have any plans to purchase within the next 72 hours. This article is intended for educational purposes only and in no way should be interpreted as investment advice.