Cisco Systems, Inc. $CSCO

Cisco Systems, Inc. $CSCO

My Investment Checklist

1. Is the company undervalued?

EV/EBIT: 12.64

EV/Sales: 3.48

Price/Book: 4.69

Cisco is a high-quality business, which trades at a large discount to the market. The company has historically grown at a moderate pace and returns a significant amount of capital back to shareholders. Notwithstanding $CSCO is facing supply chain and inflationary challenges, which has analysts worried that growth will be non-existent for the foreseeable future. Nevertheless, investors could party like it’s 1999 if the situation changes from bad to not so bad.

2. Can I easily explain what the company does?

Yes, they sell primarily communication hardware to enterprise clients. $CSCO also has a software/services offering on the equipment they sell, which makes up ~27% of sales.

3. Does the cash flow statement line up with income statement?

Yes, cashflows have been consistently higher than reported income:

Most of their excess cash went towards; share buybacks, dividends, debt repayment, acquisition costs, and capital expenditures. Outside purchases always make me uneasy and in the last 9 months $CSCO has bought 3 businesses; Opsani, Replex, and Epsagon Ltd. Upon reading each company description it’s hard to decipher if there will be any synergies with Cisco’s core business. However management would like to you to know that it’s part of their “Full-Stack Observability Strategy”. I have no clue what that word salad means, but I do know these enterprises came with a hefty price tag:

My goodness, that’s an absurd amount of goodwill! In fairness these are all software companies, so it shouldn’t surprise anyone to see a lack of assets. Additionally the acquisition costs were fairly low relative to earnings. With that said the ambiguity surrounding these investments leads me to believe they will destroy shareholder value. Moving forward investors would be wise to make sure management doesn’t keep spending on acquisitions like they’re livin’ la vida loca!

4. Is the Balance Sheet Healthy?

Total Cash: $20.11B

Total Debt: $9.42B

Current Ratio: 1.49

Cisco is sitting on a ~$10B net cash position, so it’s wouldn’t be a stretch to say their balance sheet is larger than life!

5. How profitable is the business?

Gross Margins: 63.3%

Operating Margins: 27.2%

Net Margins: 22.94%

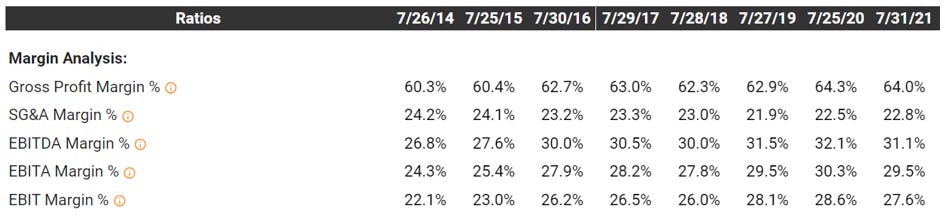

It’s clear to see that $CSCO is an outstanding business. This reflects a strong moat due to high switching costs and a well known brand. There may be some near term noise due to supply chain issues, but $CSCO has been remarkably consistent regarding profitability:

For these reasons, I would anticipate $CSCO to maintain a bootylicious margin profile for years to come!

6. What is the company’s growth potential?

10-yr Revenue CAGR: 1.4%

10-yr Operating Income CAGR: 2.84%

10-yr FCF CAGR: 3.57%

The trailing data is most likely understating Cisco’s growth potential. For example from 2012-2019, EBIT grew at 4.33% annually. Additionally $CSCO does have secular tailwinds behind them, as data center and cloud computing are expected to grow for some time. Nonetheless, Carson Daly has better odds of returning to MTV than $CSCO does of growing double digits. Furthermore $CSCO has grown primarily thru acquisitions, so it should go without saying that don’t impress me much!!!

7. Is management rewarding shareholders?

$CSCO currently offers investors a 3.33% dividend and have $17.6B remaining on their share repurchase program. With earnings expected to be flattish for the next year, Cisco should have around $13B in FCF. Because $CSCO is sitting on a net cash position most of that FCF will flow thru to equity holders. If we back out SBC that leaves shareholders with ~6.5% total shareholder yield. This number could be lower if Cisco continues buying outside companies, conversely it could be higher if they start depleting cash. If you’re an avid reader of mine you should by now that shareholder yield is my fire, the one desire! Whereas a zero capital return policy leads to nothing but a heartache!

8. How does the company stack up against their peers?

Cisco’s closest competitor is Juniper Networks Inc, $JNPR:

$JNPR EV/Sales: 2.12

EV/EBIT: 22.23

Operating Margins: 9.5%

$JNPR trades cheaper on some metrics, however it’s objectively a lower quality business. Additionally both companies return about the same amount of capital back to shareholders. However $CSCO has grown slightly faster and has a better balance sheet. For this reason I’m saying; bye, bye, bye to $JNPR!

9. What’s the counter argument?

The counter argument is that supply chain issues will cause revenues and earnings to contract for an indefinite time.

I don’t disagree with this point, particularly because a good portion of Cisco’s sourcing comes from China. Management stated that China plans on reopening by June 1st, but went on to admit there’s serious doubts supply chains ease anytime soon. The good news is that their order backlog is up 8% YOY and they will realize significant software revenues once their hardware ships out. Unfortunately $CSCO is beholden on the Chinese government which is driving shareholders crazy, they just can’t sleep!

10. Is there something I think the market may be missing?

The current multiple implies low to no growth for $CSCO, although I’m not so sure that will happen. $CSCO doesn’t have a demand problem, they have a distribution problem. Once that issue alleviates itself, I wouldn’t be surprised to see high single digit growth for a couple years. If that scenario pans out, investors are in for an S Club Party and everyone knows there ain’t no party like an S Club Party!!!

Final Thoughts:

My base case would be as follows; EBIT growing annually at 4% for the next 5 years, a 6.5% net shareholder yield per year, and a 13X EV/EBIT exit multiple. That works out to a ~12% expected IRR, which is above market but not by much. Having said that the stock is worth tracking as it’s a high quality name, which could get much cheaper if supply chain problems persist. Unfortunately the margin of safety isn’t there to meet my hurdle rate and I’m certainly not one to go chasing waterfalls!!!

***Disclosure: I have no position in the security mentioned above, nor do I have any plans to purchase within the next 72 hours. This article is intended for educational purposes only and in no way should be interpreted as investment advice