1-800-FLOWERS.COM, Inc. $FLWS

1-800-FLOWERS.COM, Inc. $FLWS

My Investment Checklist

1. Is the company undervalued?

EV/EBIT: 11.7

Price/Sales: 0.68

Price/Book: 2.92

$FLWS trades at a massive discount to the market, while offering investors double digit revenue growth. With that said 1-800-FLOWERS has profitability concerns and is objectively a below average business. Nonetheless investors could achieve outsized returns as the business is growing, returning capital back to shareholders, and trading at a historically low valuation.

2. Can I easily explain what the company does?

Yes, they are a direct-to-consumer gift business, selling mostly flowers and gourmet food gift baskets.

3. Does the cash flow statement line up with income statement?

Earnings have been extremely choppy for $FLWS, and there’s a massive discrepancy between reported earnings and operating cashflows over the last 7 quarters. This delta is approximately a $132M, which is a huge red flag. Some of this could be explained by how they account for inventories, but even being generous the numbers don’t seem to add up. It’s my belief that $FLWS is embellishing/overstating their reported earnings, which is no bueno for shareholders.

Regarding capital allocation $FLWS paid off debt, spent on capital expenditures, and bought back shares last year. I don’t have any issues with these decisions, however it’s important to note that 1-800-FLOWERS has historically acquired outside companies. Most recently buying Personalization Mall in August of 2020. For $FLWS to keep growing at double digits they will have to rely on acquisitions such as this.

4. Is the Balance Sheet Healthy?

Total Debt: $300.8M

Total Cash: $3.79M

Current Ratio: 1.4

$FLWS actually has pretty low debt for a company that is a regular purchaser of outside businesses. Furthermore they had $6.3M in net interest payment last year, while throwing off $54.5M in free cash flow. For these reasons the balance is quite healthy and 1-800-FLOWERS may be able to fund future acquisitions thru free cash flow and not debt.

5. How profitable is the business?

Gross Margins: 41.77%

Operating Margins: 6.62%

ROIC: 16.16%

10-yr Revenue CAGR: 12.4%

While $FLWS exhibits strong gross margins, their operating and net margins are frankly bad. They are forced to spend a significant amount on marketing and technology related expenses:

Moreover these costs are re-occurring and growing in nature, as an investor I would treat them the same as maintenance capital expenditures. It’s for these reasons that $FLWS trades at a discount to the market and rightfully so IMO.

6. Is management rewarding shareholders?

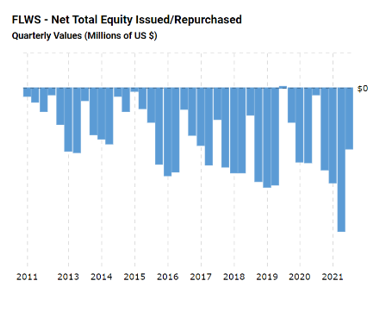

1-800-FLOWERS doesn’t offer a dividend, but they do have a $40M share repurchase plan in place. Furthermore they have a history of returning capital back to shareholders:

Moving forward it would not be unreasonable to assume ~$25M per year in buybacks. Unfortunately $FLWS is also addicted to giving out stock based compensation, awarding $10.8M in 2021 compared to $8.4M in 2020. When you back out the SBC, $FLWS is only yielding ~ 1%!

7. How does the company stack up against their peers?

I couldn’t a find a comparable publicly traded direct to consumer business for 1-800-FLOWERS. Therefore, I’m going to skip this question.

8. What’s the counter argument?

The counter argument is that margins will deteriorate and growth will slow as acquisition opportunities dry up.

Candidly I’m unsure of how many opportunities $FLWS has, but believe there’s some white space ahead as there seems to be a new direct to consumer brand being marketed to me every 2 minutes. Although, there’s some evidence that margins are likely to come down from here. For example management is guiding for 10-12% revenue growth in 2022, but only 5-8% EBITDA growth. Additionally EBIT margins have historically been ~3.5% and in the last 12 months they’ve averaged 6.6%. In fairness some of their recent acquisitions may lead to a structurally improved margin profile, but I have a hard time believing margins will expand from here.

9. Is the company unsexy, uncool, or contrarian?

$FLWS has 6 analysts covering the stock with 1 sell, 4 holds, and 1 buy rating out. Furthermore it’s in an industry I wouldn’t consider to be either hated or loved. For these reasons the stock is just meh.

10. Is there something I think the market may be missing?

The lowest Mr. Market has valued $FLWS in the last decade has been around a 10X EV/EBIT. The current valuation isn’t far off that number and management is guiding for $100M in free cash flow this year (2022). This coupled with a nearly 21% short interest and buyback plan in place, makes for a compelling set up. I’m not suggesting that a squeeze will happen but if management gets aggressive with the share repurchases, shorts will be forced to cover by buying the stock back at higher prices.

Final Thoughts:

$FLWS checks almost every quantitative box, but I don’t fully trust management. The discrepancy between cashflows and earnings are bothersome and there doesn’t seem to be a logical explanation for it. Moreover the capital return to shareholders is vastly overstated when you account for stock based compensation. Finally I prefer investing in companies who can grow organically, instead of thru mergers and acquisitions. It’s for these reasons that $FLWS is a pass for me and something I probably won’t revisit.

***Disclosure: I have no position in the security mentioned above, nor do I have any plans to purchase within the next 72 hours. This article is intended for educational purposes only and in no way should be interpreted as investment advice