Smith & Wesson Brands Inc. $SWBI

Smith & Wesson Brands Inc. $SWBI

My Investment Checklist

1. Is the company cheap?

EV/EBIT: 3.8 (this is misleading)

Price/Sales: 0.96

Price/Earnings: 12.25

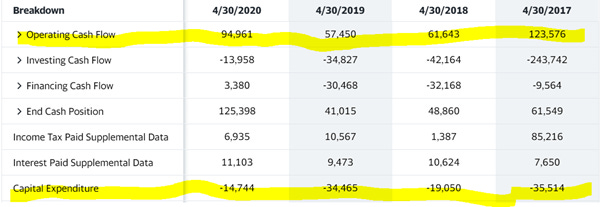

At first glance $SWBI appears to be trading at an absurdly low valuation. This is due to an outstanding 2020 where operating income tripled its historical averages:

If we normalize operating income to $100M per year the EV/EBIT would be 9.49, which is still very cheap.

2. Can I easily explain what the company does?

Yes, they manufacture and sell guns.

3. Does the cash flow statement line up with income statement?

Yes, for the most part operating income has been higher than reported earnings.

Almost all of this excess cashflow went to paying down long-term debt in 2020, as well as nearly $50M allocated towards share repurchases. I also found it interesting that $SWBI CAPEX is relatively low for a manufacturer:

This affords $SWBI a significant amount of free cash flow to either grow the business or to be distribute cash back to shareholders.

4. Is the Balance Sheet Healthy?

Total Debt: $45.4M

Total Cash: $59.68M

Current Ratio: 1.92

Really no need to spend much time on this question, $SWBI has an ELITE balance sheet! They are likely in the 90th percentile for all balance sheet metrics and solvency is by no means a concern for shareholders.

5. How profitable is the business?

Gross Margins: 40.67%

Net Margins: 8.74%

ROE: 25.19

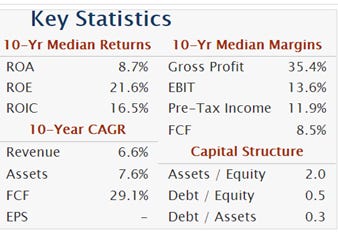

10-year Revenue CAGR :6.6%

2020 was an exceptional year for $SWBI, so it’s best to look at their 10-yr averages in order to get a better idea of what shareholders can expect in the future:

Surprisingly $SWBI profitability metrics actually hold to the TTM numbers. The company is less profitable than the average business in the S&P 500, but the disparity isn’t as wide as their valuation would indicate.

6. Is management rewarding shareholders?

$SWBI management team approved their first dividend to be paid on 9/17/2020. The current yield only 1.05%. Be that as it may management also recently approved a $100M share repurchase program, which is over 10% of their current market cap. All share repurchase plans come with strings attached, but total shareholder yield should be well above the market average moving forward. Moreover $SWBI has next to no debt, so there’s plenty of room to return more capital to shareholders if management decides to go that route.

7. How does the company stack up against their peers?

The only publicly traded competitor I found for $SWBI is Sturm Ruger & Co. $RGR

$RGR Price/Sales: 2.14

EV/EBIT: 9.24

Gross Margins: 33.65%

$RGR trades at a higher valuation than $SWBI and has historically produced less impressive cashflows, but they offer a higher dividend yield. Having said that $RGR didn’t buyback any shares in 2020 and their dividend yield is a bit goosed due to a large special dividend they declared last year. I prefer $SWBI over $RGR as the valuation is more attractive and their future prospects look better IMO.

8. What’s the counter argument?

The biggest risk $SWBI faces is political risk, with democrats controlling the Presidency, house, and senate. Democrats seem to be on a crusade to implement gun control reform, if not totally ban them ie; Beta O’Rourke (that spelling was intentional).

Putting aside the fact that this is a totally illogical argument, criminals are gonna find a way to get their hands on guns whether they are legal or not. I’m a bit dismissive that any new laws will be put into place regarding gun control. The fact of the matter is politicians are by and large the most useless group of individuals on planet earth. No matter what side of the isle you fall on politics is mostly empty words and political posturing.

Furthermore even if a policy is passed, an unintended consequence may be that gun sales actually increase. Similar to how alcohol consumption went up after prohibition was implemented. It’s also important to disclose my biases here, I’m a libertarian (pretty much a conservative). However, I’ve never owned a gun in my life and don’t plan on every owning one.

9. Is the company unsexy, uncool, or contrarian?

$SWBI has 6 analysts covering the stock with; 3 buys, 1 outperform, and 2 hold ratings out. I was actually pleasantly surprised to see analysts sticking their neck out on a sin stock like $SWBI. Having said that our society has grown softer than tissue paper in the last decade and due to the ever-mounting number of SJWs, $SWBI is no doubt unsexy and uncool.

10. Is there something I think the market may be missing?

$SWBI is priced well below its intrinsic value in my estimation. Mr. Market has to be pricing in either revenue declines or margin compression for the valuation to make sense. I know I just went on a big rant regarding the pussification of American, but I respect the shit out of Mr. Market. If regulation comes $SWBI could be worth only its book value, which is ~ 23% of the current market cap.

If however regulation doesn’t come $SWBI is positioned fabulously. They paid off almost all their debt and are throwing off an absurd amount of free cash flow. This stock could easily 3X if they grow revenues at a meager 6% annually.

Final Thoughts:

The biggest question investors have to ask themselves is whether of not regulation is coming for the gun industry. If you don’t think so, the stock is a screaming buy IMO. Personally, I would like a bit more clarity coming from government regarding any potential reform. This likely won’t happen until after Covid-19 has fully run its course. The obvious issue with this line of thinking is that investors could miss a massive run up, due to the uncertainty. I’m willing to miss out on those returns, as I think future political posturing may lead to an unwarranted selloff in $SWBI. Be that is it may, the stock is definitely worth tracking as it does offer an asymmetrical risk/return.

***Disclosure: I have no position in the security mentioned above, nor do I have any plans to purchase within the next 72 hours. This article is intended for educational purposes only and in no way should be interpreted as investment advice.